Cards vs APMs in Europe: Finding the Right Balance

Learn how to master the mix of cards and APMs to boost European conversions.

Europe’s payment sector is evolving fast. While card payments remain a core part of commerce, alternative payment methods (APMs) have become increasingly important for businesses seeking to convert customers across different European markets.

From Apple Pay and Google Pay in the UK, to MB Way in Portugal and BLIK in Poland, consumer payment preferences vary widely. For merchants, the challenge isn’t choosing between cards and APMs, it’s knowing how to combine them effectively.

In this article, we’ll explore cards versus APMs in Europe, explain what alternative payment methods are and look at how businesses can build a payment strategy that better aligns with European payment preferences.

The Role of Cards in Europe’s Payment Ecosystem

Cards still play a major role across Europe. Debit and credit cards are widely accepted, particularly in markets like the UK, Ireland, France and Spain. For international e-commerce, card processing remains one of the most reliable ways to accept payments from global customers.

Cards offer clear benefits:

- Familiarity and trust for consumers.

- Strong fraud protection and dispute frameworks.

- Easy support for subscriptions and recurring payments.

- Global scalability.

However, despite their reach, cards aren’t always the preferred option. In many European countries, customers actively choose alternative methods of payment that feel more local, faster, or more secure.

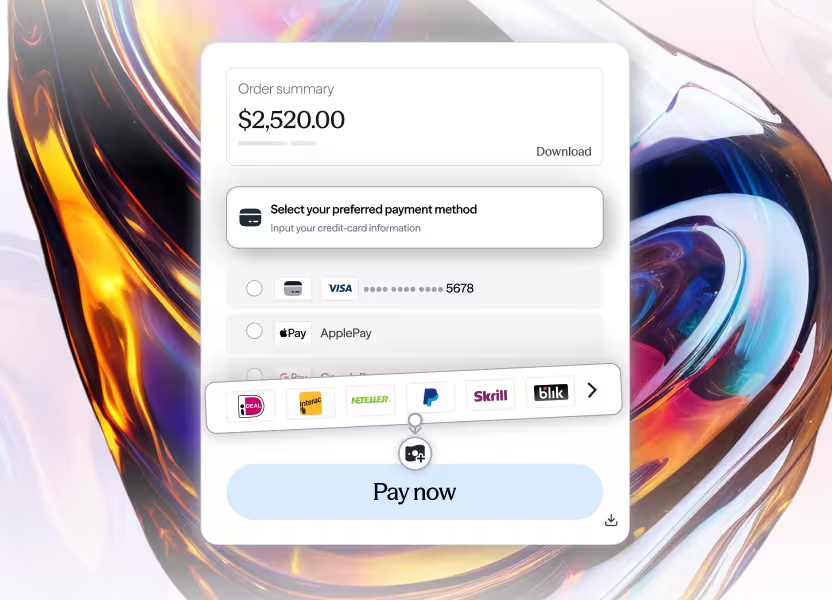

What Are Alternative Payment Methods?

So, what are alternative payment methods? APMs are any payment options outside of traditional credit and debit cards. They are often built around local banking infrastructure, mobile technology or digital wallets.

Common types of alternative payment methods include:

- Digital wallets like Apple Pay and Google Pay.

- Bank-based payment schemes such as iDEAL and BLIK.

- Mobile-first local solutions like MB Way.

- Account-to-account payments enabled by Open Banking.

These methods reduce friction at checkout by allowing customers to pay using tools they already trust and use daily.

The Rise of Global Alternative Payment Methods

APMs are growing faster than cards across much of Europe. In some markets, they dominate online payments entirely.

Examples include:

- BLIK in Poland, which enables instant bank payments through mobile banking apps.

- MB Way in Portugal, a mobile payment method deeply embedded in everyday spending.

- Apple Pay and Google Pay, which bridge the gap between cards and wallets by offering fast, secure mobile checkout.

These have grown beyond niche solutions. Global alternative payment methods have become increasingly valuable for merchants operating cross-border or targeting multiple European countries.

From a business perspective, APMs can also offer lower processing costs, faster settlement and reduced chargeback exposure compared to cards.

Cards, APMs and iGaming Payments

In regulated markets, iGaming payments place even greater emphasis on speed, trust and localisation. Players expect instant deposits and fast withdrawals, which is why APMs such as Apple Pay, Google Pay, BLIK and MB Way are increasingly popular in online gaming and betting platforms. Combining secure card processing with local alternative payment methods helps iGaming operators improve player retention while meeting compliance and risk requirements.

Alternative Payment Methods UK: Cards Plus Wallets

The UK remains a card-heavy market but APM adoption continues to accelerate. British consumers are increasingly comfortable using digital wallets and alternative methods of payment, particularly on mobile.

UK customers often switch between cards and APMs depending on convenience. If a merchant only offers card payments, they may lose customers who prefer one-click wallet payments or bank-based options.

A hybrid approach is now the norm in the UK market.

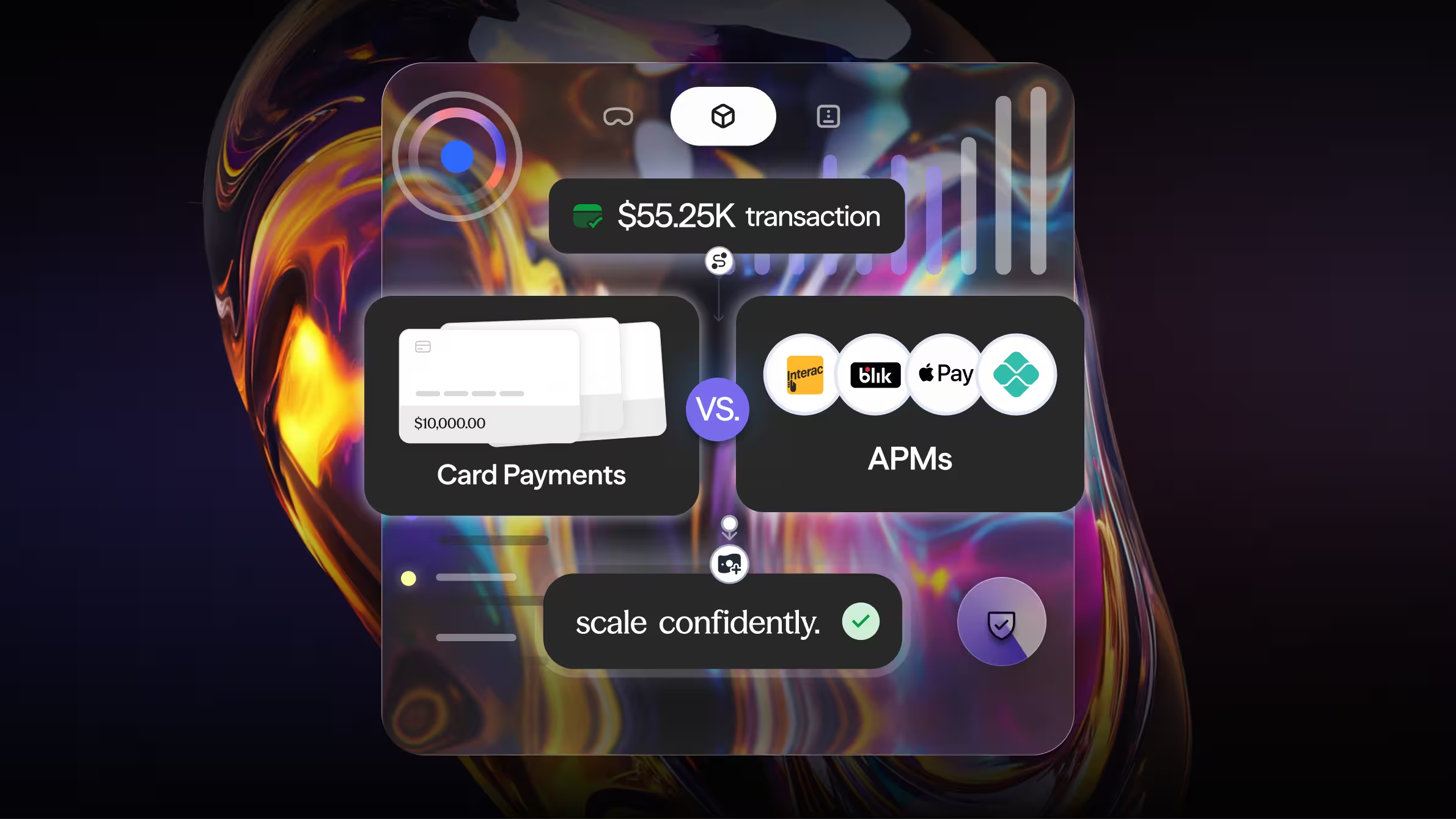

Cards vs APMs: Different Strengths, Same Goal

Cards such as Visa and Mastercard and APMs serve different use cases.

Cards work best for:

- International and cross-border customers.

- Subscriptions and recurring billing.

- High-value purchases.

APMs work best for:

- Local European markets.

- Mobile-first consumers.

- Faster checkout with fewer steps.

For example, a Polish customer may prefer BLIK over entering card details, while a Portuguese shopper may trust MB Way more than a credit card. At the same time, Apple Pay and Google Pay allow card-based payments with the speed and ease of a wallet.

The goal isn’t to replace cards but to support customer choice.

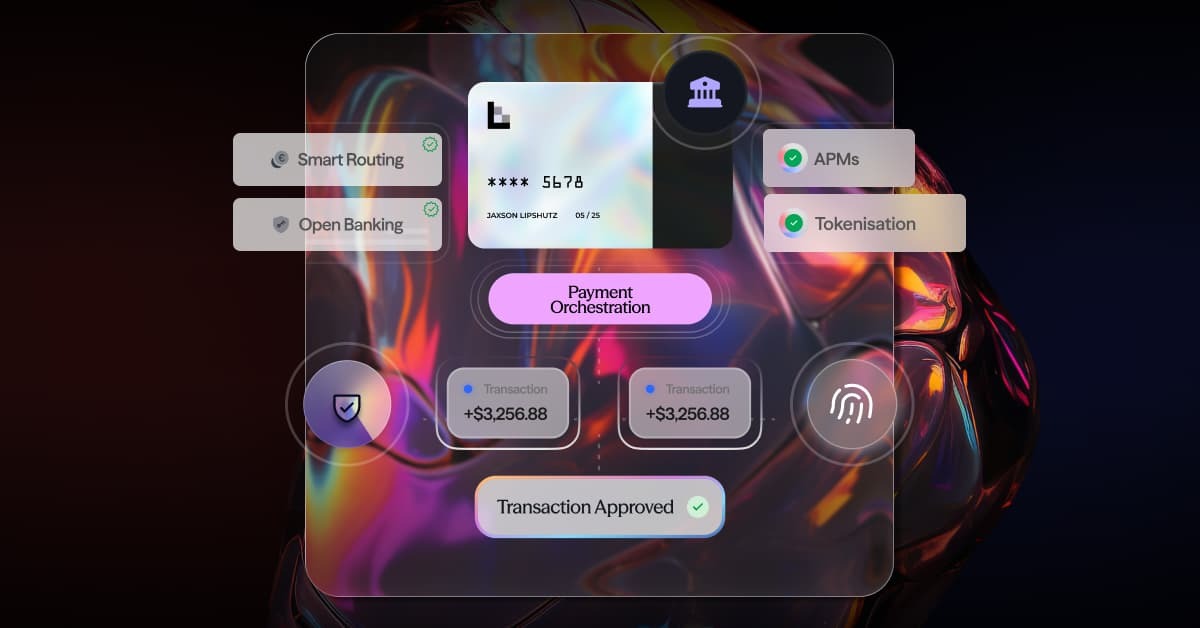

Why Payment Choice and Orchestration Impacts Conversion Rates

Payment friction is one of the biggest reasons for checkout abandonment. If customers don’t see their preferred payment method, they’re far less likely to complete the purchase.

This is where payment orchestration plays a critical role. By intelligently routing transactions and offering the right mix of card processing and alternative payment methods, businesses can optimise acceptance rates while keeping the checkout experience seamless.

An effective payment orchestration strategy may helps to:

- Increase checkout conversion rates.

- Improve customer trust through familiar payment options.

- Reduce cart abandonment.

- Support expansion into new European markets.

This is especially important for e-commerce, platforms and subscription-based businesses operating across borders, where payment preferences vary significantly by region.

Building the Right Balance for Your Business

To create an effective European payment strategy, businesses should focus on:

- Localisation: Understand which APMs dominate each target market.

- Flexibility: Support both cards and alternative methods of payment without creating operational complexity.

- Scalability: Choose a provider that supports global alternative payment methods as your business grows.

- User experience: A fast, simple checkout is just as important as pricing or product.

A unified payment solution that brings cards and APMs together is often the most efficient approach.

Power Your Payments with finera.

Cards and APMs aren’t opposing forces but complementary tools. In Europe’s diverse payment landscape, businesses that offer both are better positioned to convert customers, scale internationally and stay competitive.

If you’re operating in ecommerce or iGaming and whether you need card processing or local APMs, the right payment technology partner matters.

finera. helps businesses navigate payment ecosystems with tailored solutions for payment technology, alternative payment methods, and card processing across Europe and beyond.

Get in touch with finera. today to build a payment strategy that works for your customers and your growth.

Frequently Asked Questions

Alternative payment methods are non-card payment options such as Apple Pay, Google Pay, bank transfers, mobile wallets and local payment schemes like BLIK and MB Way.

European consumers prefer local and mobile-first payment options, making APMs essential for improving conversion rates and reducing checkout friction.

Popular APMs include Apple Pay, Google Pay, BLIK in Poland, MB Way in Portugal, PayPal, and Open Banking-based bank transfers.

Yes, card payments remain important for cross-border transactions, subscriptions and higher-value purchases, especially in markets like the UK.

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!