When Should You Add APMs to Your Checkout? A 5-Step Decision Guide

5-step guide for adding local payment methods to your checkout to improve conversions.

The way customers pay online is evolving at speed. While credit and debit cards remain important, the rise of alternative payment methods (APMs), including digital wallets, bank transfers, real-time payments and buy-now-pay-later (BNPL) services, are reshaping the global e-commerce landscape.

For merchants, especially those selling cross-border, deciding when to add local payment methods is a decision that affects not just conversion rates, but customer trust, brand loyalty and operational efficiency. Get it right, and you open your checkout to a wider customer base. Get it wrong, and you risk higher abandonment rates and slower growth.

Are your current checkout options really keeping pace with how your customers want to pay?

This guide offers a data-driven, five-step framework for deciding if, when and how to integrate APMs into your checkout as part of a broader online checkout optimisation strategy.

Step 1: Analyse Your Current Payment Data

The first step in any APM adoption strategy is knowing exactly how your customers are paying today and where you are losing them.

Dig into your payment analytics to identify:

- Decline rates by payment method and geography: If your card declines are higher in certain regions, it may indicate the need for local payment methods.

- Abandonment rates at the payment stage: Sudden drop-offs after customers see the checkout screen are often tied to a lack of preferred payment options.

- Device preferences: Mobile-first customers often prefer digital wallets over manually entering card details.

- Payment method distribution: Understanding which methods your customers currently use can guide which APMs to prioritise.

Merchants expanding into Southeast Asia, for example, often see card decline rates spike because customers there overwhelmingly prefer wallets like GCash or Maya. Without offering those, your checkout optimisation efforts are already on the back foot.

Step 2: Understand Market Preferences Before Adding Local Payment Methods

Payment behaviour is highly regional. What works in one market may fail in another. Some countries have high card adoption, while others are dominated by local payment methods and bank-based solutions.

Before rolling out new APMs, research the top payment methods in your target markets.

- Which payment methods account for the majority of ecommerce transactions in the market?

- What is the split between cards and APMs?

- Are there regulatory or compliance factors tied to certain payment types?

For example:

- Netherlands: iDEAL accounts for over half of online transactions.

- Brazil: PIX dominates local e-commerce payments.

- Philippines: Digital wallets like GCash and Maya lead in both urban and rural adoption.

Failing to integrate these local payment methods can mean instantly losing market share to competitors who do.

Step 3: Assess the Conversion Impact of Alternative Payment Methods

The strongest reason for adding APMs is improving conversion rates. Customers who can’t pay their preferred way often leave without completing the transaction and may not return.

When implemented strategically, APMs can:

- Reduce payment friction, especially for mobile-first shoppers.

- Increase approval rates by routing transactions through local acquiring banks.

- Boost customer trust by showing familiar, secure options at checkout.

For example, adding Apple Pay or Google Pay can cut checkout time to seconds, reducing the chance of drop-off. In high-growth markets, adding local payment methods to improve conversions can be the difference between breaking into the market or failing to gain traction.

The aim is selective integration, focusing on the payment methods most aligned with your APM adoption strategy for global merchants.

Step 4: Calculate ROI and Operational Impact

The benefits of alternative payment methods for e-commerce are clear, but each new method adds complexity. The operational and financial implications can include:

- Integration costs for development and testing.

- Ongoing maintenance with each provider.

- Additional fraud management rules for specific APMs.

- Settlement and reconciliation processes that vary by provider.

- Compliance requirements, particularly for bank-based payments in regulated markets.

If you are already working with multiple PSPs, managing APMs across them can quickly strain engineering resources.

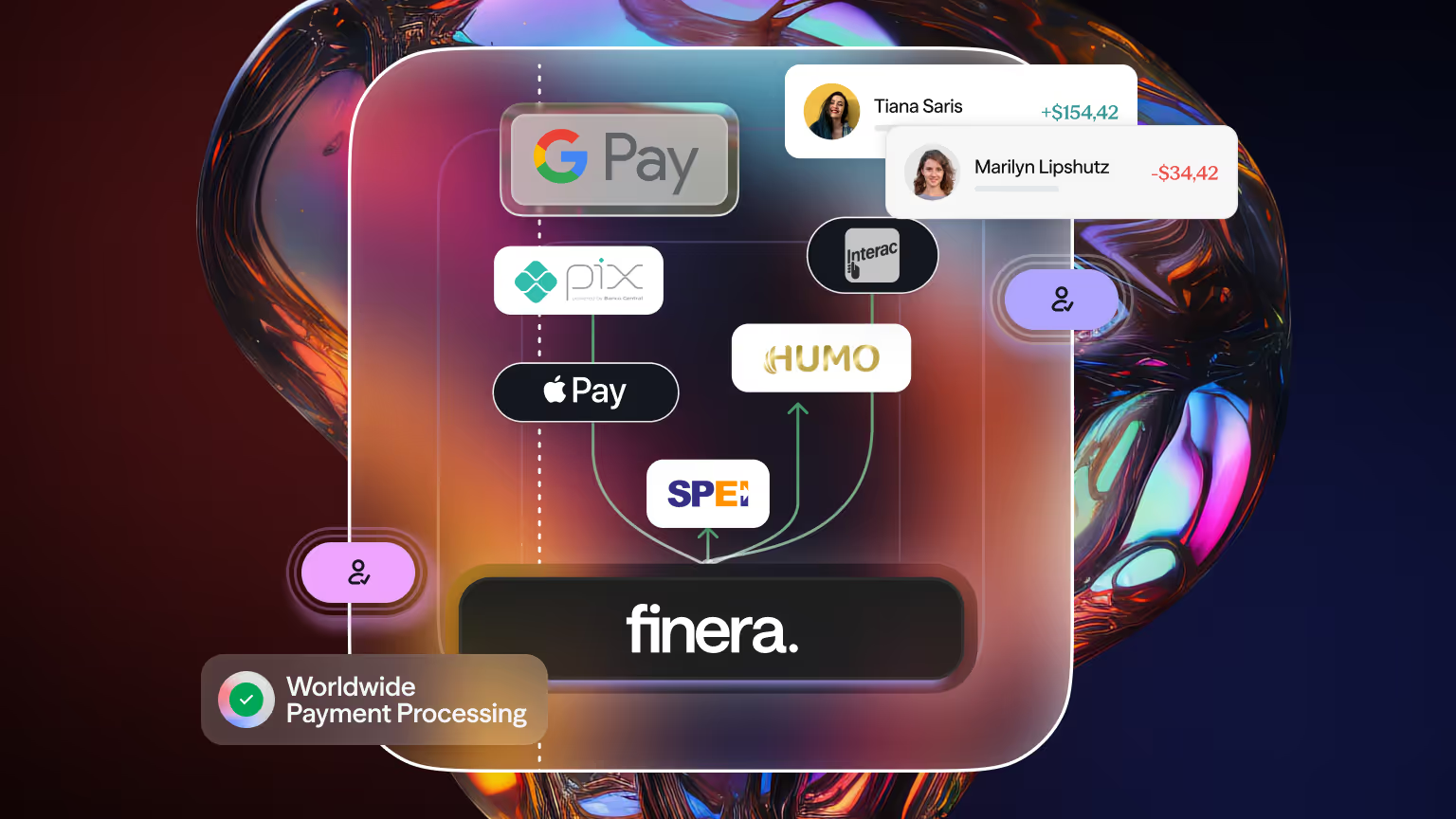

A payment orchestration platform can simplify this by:

- Connecting you to multiple APMs through a single API.

- Routing payments intelligently based on cost, performance or geography.

- Unifying reporting and reconciliation across all providers.

Factoring in both conversion gains and operational efficiency will give you a clear picture of the ROI.

Step 5: Choose the Right Integration Approach

Why rebuild your payment stack every time a new APM rises in popularity, when you could integrate once and adapt quickly?

There are three main ways to add APMs:

- Direct integration with the payment provider, highest control but most complex.

- Through your PSP, fast but limited to their network.

- Via a payment orchestration platform, which combines flexibility with simplicity, letting you test and deploy new payment methods without rewriting your entire payment stack.

For global merchants, orchestration is often the fastest way to implement and scale alternative payment methods without heavy engineering investment.

The Cost of Delaying APM Adoption

Delaying the decision to add APMs can cost you market share, especially in regions with low card penetration. Without supporting local wallets, merchants face immediate conversion losses.

Even in mature markets, APM usage is growing fast. In the UK and US, the adoption of Apple Pay and Google Pay continues to rise, particularly among mobile-first shoppers. Failing to keep up risks losing relevance.

Future-Proofing Your Checkout with Flexible APM Integration

Payment preferences are constantly evolving. APMs popular today may be replaced by faster, more convenient options in the near future. Businesses need the flexibility to test and roll out new methods quickly.

This is where payment orchestration plays a strategic role, enabling merchants to add, remove or optimise APMs without costly re-engineering. For CTOs and product teams, that means keeping the checkout aligned with market trends while protecting the product roadmap from disruption.

When Should Businesses Add APMs?

The question "when should businesses add APMs to their checkout" depends on data, market priorities and operational readiness.

If payment analytics reveal that customers are abandoning checkout due to a lack of preferred payment options, particularly in key growth markets, then the answer is simple: act now.

Adopt the most in-demand local payment methods, ensure they are integrated in a way that supports scalability and monitor their impact on conversion. Done right, adding alternative payment methods is a growth strategy.

At finera., we help businesses integrate alternative payment methods seamlessly with smart routing, multi-currency support and 24/7 service. Talk to our team today to see how APMs can accelerate your global strategy.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!