APMs That Drive Conversions in eCommerce Markets and Beyond

Boost eCommerce conversions with APMs your customers trust. Here's how to do it the smart way.

Why do customers fill their shopping carts, only to disappear at the checkout?

You have invested in traffic, optimised your UX and nailed your product-market fit. But when it comes to the final click, conversion rates plummet.

The main reason? You are not offering the payment methods your customers trust.

Traditional cards are not enough anymore. Today’s global eCommerce shopper expects Alternative Payment Methods (APMs); digital wallets, local bank transfers, real-time payments and region-specific mobile wallets.

And this isn’t just about offering more options, it's about payment orchestration: the ability to intelligently route, localise, and optimise every transaction using the right method, in the right market, at the right moment.

In this article, we break down the APMs that directly boost conversions, explain how payment orchestration supports a better checkout experience and show how to implement it without complexity.

What Are Alternative Payment Methods (APMs)?

APMs are payment methods that fall outside the traditional debit and credit card systems. These include:

- Digital wallets (e.g., Apple Pay, Google Pay)

- Bank transfers (e.g., Open Banking, Instant Bank Transfer)

- Mobile money (e.g., GCash, Maya)

- QR-based systems (e.g., Thai QR)

- National instant payment networks (e.g., PIX in Brazil, SPEI in Mexico)

These methods are often region-specific, deeply integrated into local consumer behaviour and tailored to mobile-first experiences. While credit cards remain widely used in some countries, APMs are dominating in others, especially in emerging markets and among younger demographics.

Why APMs Improve Checkout Conversion

Cart abandonment is often blamed on slow load times, surprise fees or confusing site design. But one of the most commonly overlooked reasons is much simpler: the payment method isn’t right.

When shoppers reach the checkout and don’t see a method they recognise or trust, hesitation kicks in. That hesitation often turns into abandonment.

Alternative Payment Methods (APMs) play a crucial role in removing that friction. Digital wallets and instant bank transfers streamline the process, often enabling one-click checkouts. Many APMs are also designed with mobile in mind, making them ideal for the growing number of consumers shopping on their phones.

Beyond convenience, there’s trust. In many regions, customers prefer government-backed systems or national bank transfer networks over international cards. And with real-time or near-instant settlement, APMs reduce perceived risk and improve the overall payment experience.

The result for merchants? Fewer barriers, more completed checkouts and better conversion rates.

Regional APMs That Power Conversions

Not all APMs perform equally. The key is relevance, offering payment methods that match your customers’ expectations in each market.

North America

- Apple Pay & Google Pay: Widely used among mobile shoppers worldwide, especially in the U.S. and Canada. One-click payments improve conversion speed and reduce errors.

- Interac (Canada): A real-time bank-based transfer system trusted for both peer-to-peer and merchant payments.

Latin America

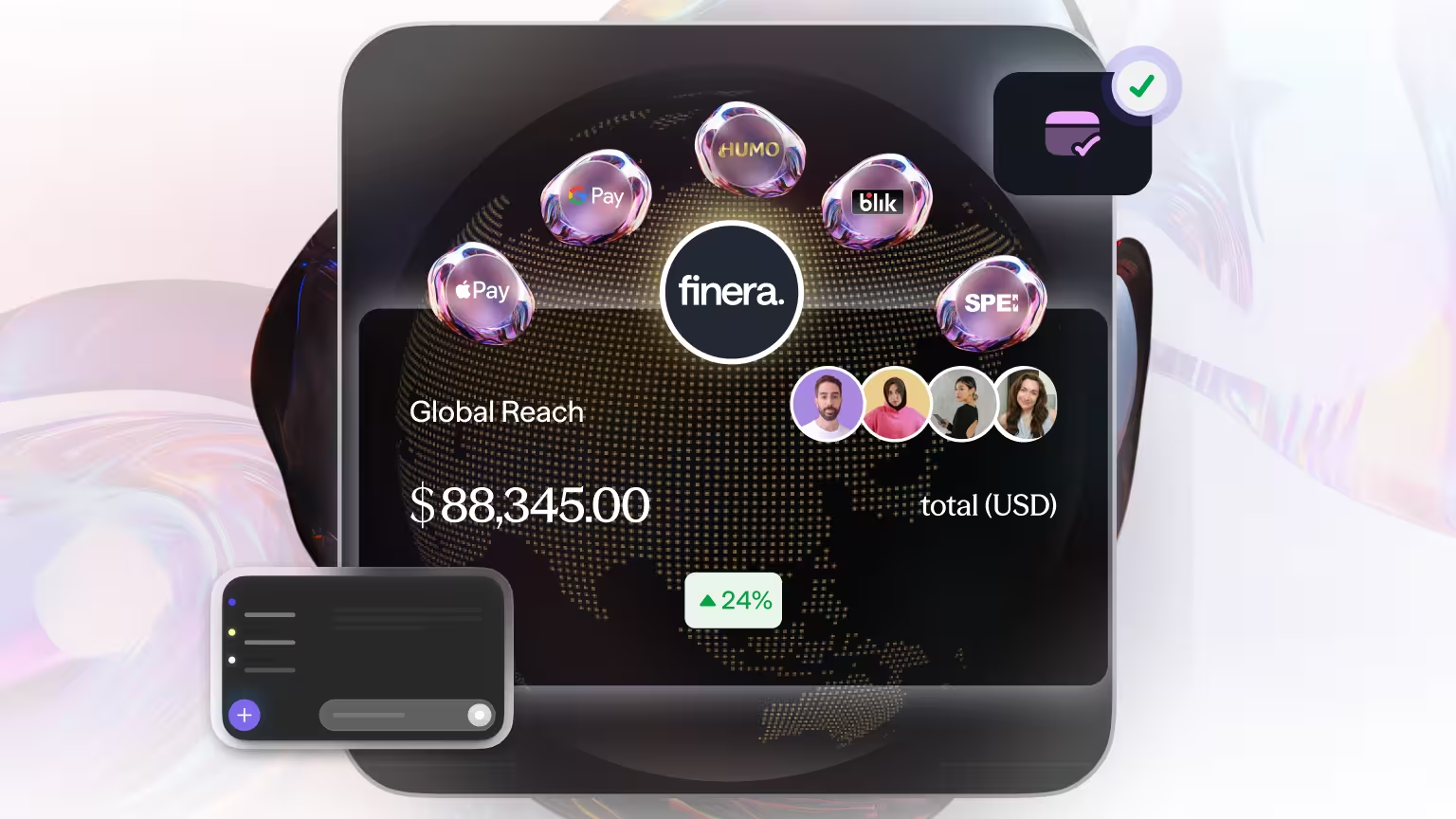

- PIX (Brazil): Developed by Brazil’s Central Bank, PIX is an instant payment system embedded in consumer life. It enables payments in seconds with no fees and is used by over 70% of the population.

- SPEI (Mexico): SPEI allows users to pay directly from their bank accounts. It’s secure, widely adopted, and supported by major financial institutions.

Europe

- Open Banking (UK/EU): Enables secure payments directly from bank accounts, -eliminating the need for card details. Trusted in financial services and increasingly adopted in retail.

- BLIK (Poland): A mobile payment standard integrated with Polish banking apps, allowing code-based or QR-based payments.

Asia-Pacific

- GCash (Philippines): One of the country’s leading mobile wallets, enabling quick payments via mobile number or QR.

- Maya (Philippines): A fast-growing mobile wallet and digital bank popular with younger demographics.

- Thai QR Bank Transfer: Government-supported and widely used in Thailand for both online and in-person payments.

- PayID (Australia): Instant bank payments linked to phone numbers or email addresses. Common in B2C and P2P payments.

Central Asia & Emerging Markets

- UZCARD & HUMO (Uzbekistan): Local card schemes are essential for merchants targeting Uzbekistan. Trusted by consumers and compliant with local regulations.

- Havale (Turkey): A preferred method for domestic bank transfers, particularly for older or non-card-using demographics.

Offering even a few of these methods can make a significant difference in conversion rates, especially if you are targeting specific countries or regions.

The Business Case for APMs

Beyond a better customer experience, APMs make strong business sense.

- Higher approval rates: Local methods often integrate directly with banks, reducing the chance of failed payments.

- Lower processing costs: Many APMs have lower fees compared to card networks.

- Increased Average Order Value (AOV): Customers who trust the checkout process are more likely to spend more.

- Reduced fraud: Bank-linked systems and tokenised wallets lower the risk of chargebacks and card fraud.

Merchants that localise their payment experience consistently see improvements in conversion metrics, especially in mobile-first and emerging markets.

Implementation: How to Add APMs Without Adding Complexity

Adding dozens of local payment methods sounds daunting but it doesn’t have to be. The best approach is to work with a partner that consolidates global APM coverage under one integration.

When evaluating a solution, look for:

- Pre-built APM integrations across key markets

- Real-time payment capabilities

- Mobile optimisation

- Tokenisation and fraud prevention features

- Transparent pricing per transaction

This is where finera. makes a measurable difference.

Don’t Let Payments Be the Reason You Lose a Sale

The final stage of the buyer journey is also the most fragile. No matter how compelling your product is or how beautifully designed your online store may be, if customers can’t pay the way they want to, they’ll leave. According to the Baymard Institute, the global average cart abandonment rate is just over 70%, with mobile abandonment rising as high as 85%, often due to slow, confusing, or limited payment options.

Increasingly, what customers expect at checkout is a choice of Alternative Payment Methods (APMs), from mobile wallets and bank transfers to region-specific services like PIX in Brazil or GCash in the Philippines. APMs already account for more than 55% of global eCommerce transactions, a figure projected to reach nearly 82% by 2026, according to Worldpay’s Global Payments Report.

The business case is clear: offering the right mix of local and mobile-first APMs can improve conversion rates by 20–30% or more, especially in regions where traditional card payments are less common or less trusted. Payments are no longer just a backend function, they’re a frontline driver of revenue and retention. And APMs are no longer fringe, they’re the preferred standard in some of the world’s fastest-growing digital commerce markets.

Ready to Offer APMs That Convert? Talk to finera.

At finera., we help businesses increase revenue by supporting the payment methods that customers trust most. If you are expanding into Brazil, Southeast Asia or Eastern Europe, our platform gives you access to the world's top-performing APMs through a single integration.

From Apple Pay to PIX, GCash, Maya, Open Banking and many more, finera. enables fast, secure and frictionless checkouts tailored to your markets.

Stop losing conversions at the final step. Start offering the payment options your customers already trust. Talk to our team.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!