APMs: Why Businesses Need More than Just Cards

Cards work. But APMs boost new payment growth. Here's why you need both in your strategy for 2025.

Most businesses still rely on cards to drive online transactions. And for years, that worked. But habits have changed.

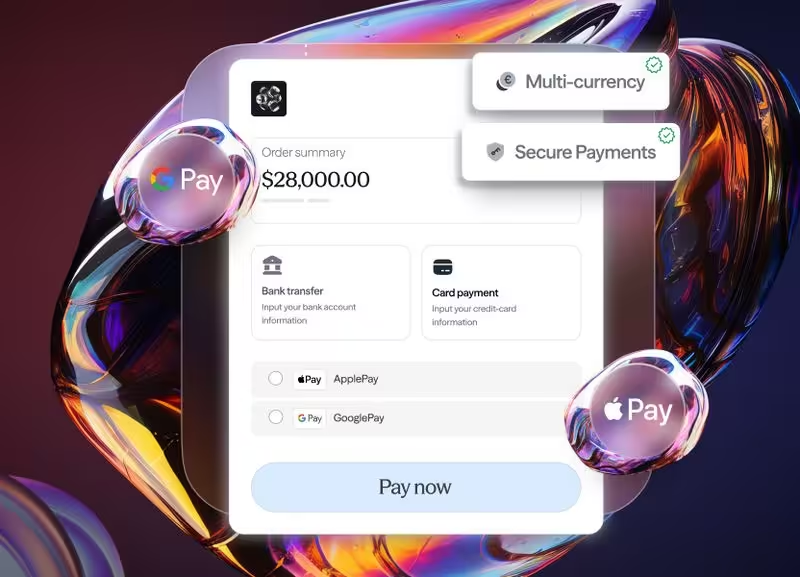

Your customers don’t just want a card input field. They expect to pay with the tools they already use and trust, from Google Pay on their phones to direct bank transfers or mobile wallets popular in their region.

And when those options aren’t there, many simply leave.

If you see checkout drop-offs, inconsistent approval rates, or rising processing costs, cards alone may no longer be enough.

Offering the right APMs (alternative payment methods) can help you reduce friction, increase success rates, and stay relevant in global markets.

Cards Cover the Basics. APMs Cover the Gaps

Cards still play a major role in e-commerce. But they are no longer representative of how most people pay online.

In 2024, digital wallets accounted for over 47 billion dollars in global transactions, with the market projected to grow to USD 56.9 billion in 2025, a nearly 20% year-on-year increase (The Business Research Company).

This growth signals that mobile and app-based payments are becoming the standard, not the alternative. If your checkout is card-only, you are missing a growing share of your potential revenue.

3 Reasons Why APMs Improve Performance

Adding alternative payment methods isn’t just about variety. It directly improves business outcomes.

1. Higher Approval Rates

In high-risk sectors or in cross-border transactions, card approvals can be inconsistent. APMs like open banking or local bank transfers skip intermediaries, increasing the chances of a successful transaction.

If a customer in Europe prefers a direct bank-to-bank payment rather than entering long card details, offering that option keeps the sale alive.

Open banking is no longer a niche offering. According to Global Market Insights, by 2024, the global open banking market had reached USD 28.2 billion, with expected strong growth through 2034.

2. Lower Cart Abandonment

A customer browsing on their phone might expect to complete their purchase with Apple Pay or Google Pay. No typing, no delays. If that’s not an option, they often won’t come back.

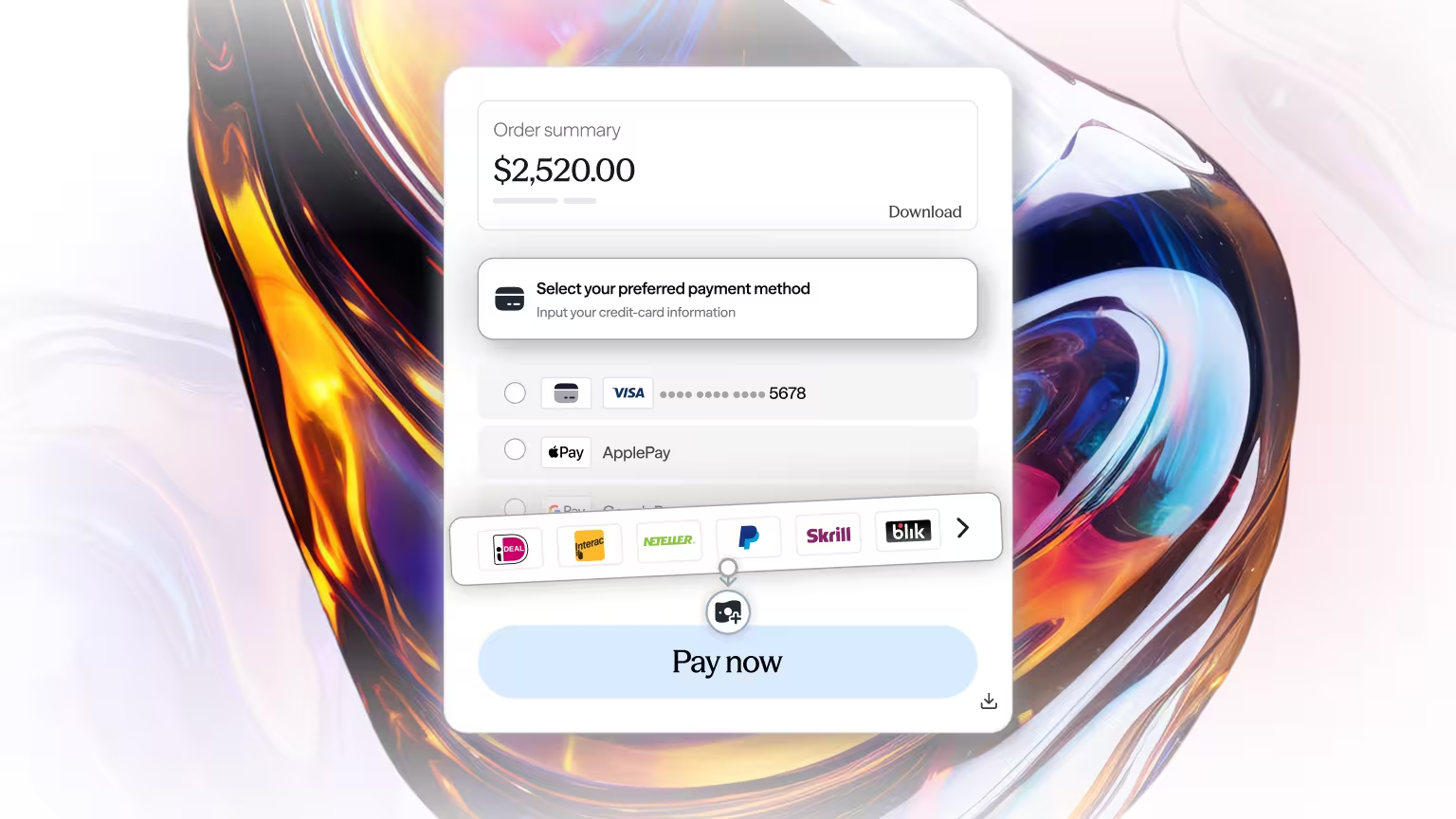

And for users in regions like Brazil or Canada, methods like Pix or Interac are more trusted and efficient than entering card details.

Providing localised options improves completion rates, especially in mobile-first markets.

3. Faster, Real-Time Payments

Real-time methods offer speed and reliability. Global data from ACI Worldwide shows that 266.2 billion real-time payment transactions were processed in 2023, reflecting a 42% year-on-year increase.

This sharp growth reflects how user and merchant demand for instant confirmation continues to rise, particularly in retail and high-volume sectors.

Applying APMs in the Real World

Let’s say your business is expanding into Latin America. Card acceptance in the region can vary, especially for international cards. But with the rise of real-time systems like Pix, local customers expect fast and secure payments.

Now, imagine your checkout doesn’t support Pix. Your ad spend works. Traffic converts. But payments fail or bounce because the expected method isn’t there.

The same applies to mobile-first users. If you aren’t offering native options like Google Pay or Apple Pay, you are adding unnecessary steps to a process that should be instant.

APMs Work Best With Cards, Not Instead of Them

Some businesses worry that adding APMs means replacing what’s already working. It doesn’t.

Cards still have a role. But APMs fill gaps that cards can’t:

- Where cards are declined

- Where local preferences dominate

- Where mobile or real-time experiences matter

Offering both means you’re covered for the users who prefer traditional methods and for those who don’t.

And with smart payment orchestration, each transaction can be routed in real time to the method most likely to succeed.

Know When It’s Time to Expand

Ask yourself:

- Are you growing in markets where cards aren’t the first choice?

- Are you seeing higher declines in cross-border transactions?

- Are mobile users bouncing at the payment stage?

- Are you relying too heavily on one payment method?

If you answered yes to any of the above, APMs can help fix the problem before it affects your bottom line.

Make the Right Payment Decisions with finera.

Cards aren’t going away. But relying on them alone puts limits on your growth, especially if your customers prefer to pay another way.

At finera., we help you access the APMs that make a difference. From mobile wallets and open banking to real-time bank transfers, all through one smart platform.

Want to reduce friction and increase payment success? Talk to finera. today to see how alternative payment methods can support your growth, globally and intelligently.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!