Apple Pay vs Google Pay: Breaking Down the Differences

Key differences between digital wallets for contactless payment with Apple Pay and Google Wallet.

Mobile payment systems are everywhere, but they don’t all work the same way.

Apple Pay and Google Pay are two of the most widely used mobile payment systems. They offer secure contactless payments, digital wallets, and money transfers. On the surface, they may look similar, but their features, structure, and design choices make a big difference in how they work. For businesses exploring mobile-enabled checkout, loyalty integration, or contactless customer experiences, understanding how these wallets function is essential.

Here’s a clear look at what each service offers, how they handle your information, and the key differences between them.

Platform Compatibility

Let’s start with the basics.

Apple Pay

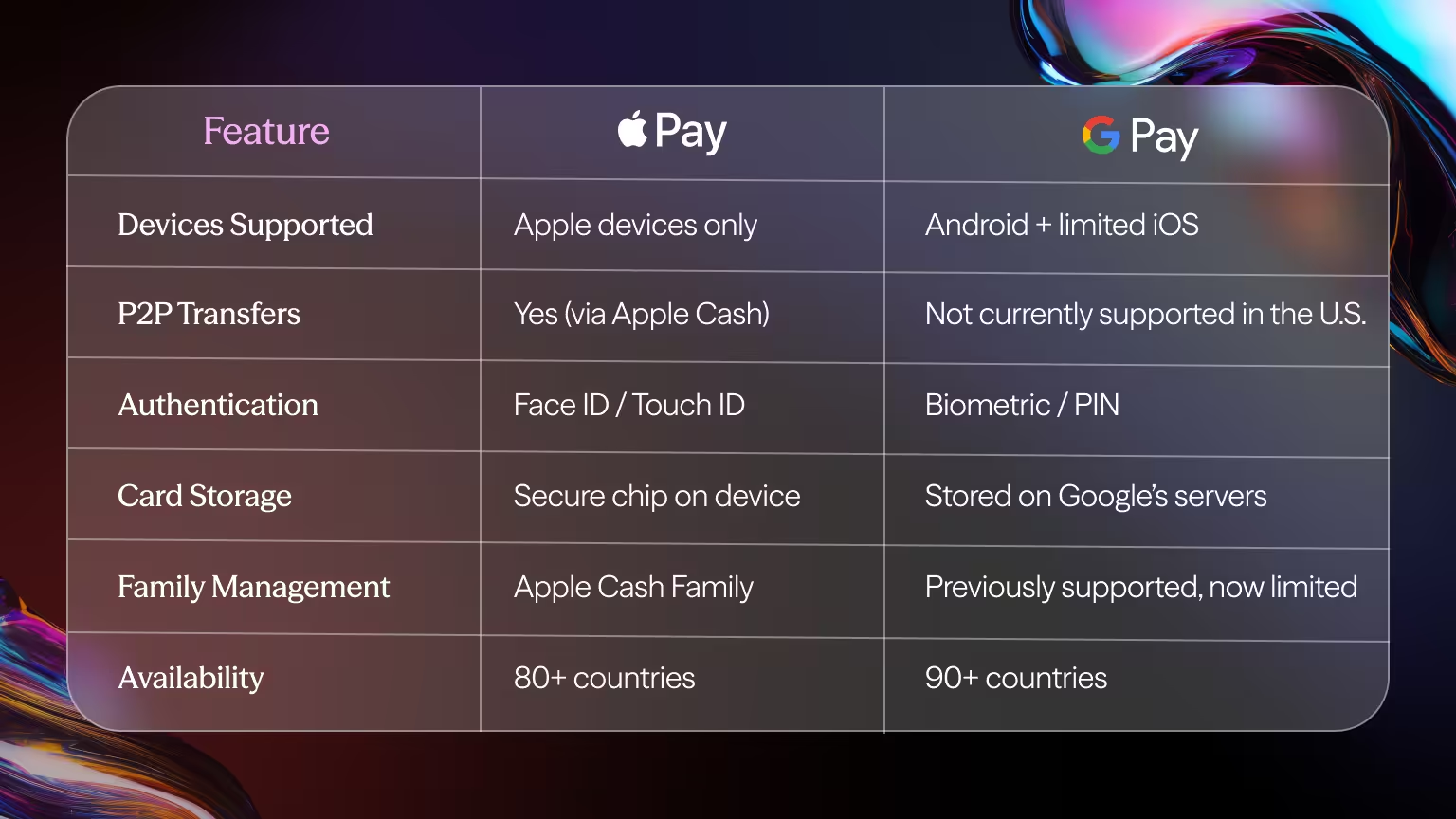

Works exclusively on Apple devices. It’s available on iPhones with Face ID or Touch ID, iPads, Apple Watches, and Macs with biometric authentication. If you are using Apple hardware, Apple Pay is already built in.

Google Pay

Designed specifically for Android. It works across a wide range of phones and smartwatches, and there is a version for iOS too. On iPhones, though, you won’t get contactless functionality.

That difference matters. Apple controls the hardware and software behind Apple Pay. Google’s broader support means more device options, especially on older hardware.

How the Wallets Work

Apple Wallet and Google Wallet do similar jobs. Both store:

- Payment cards.

- Tickets and passes.

- Transit cards.

- Loyalty cards.

- Government IDs (in supported regions).

But there are some key distinctions.

Apple Wallet is where you manage all of these within the Apple ecosystem. It also supports Apple Cash, which allows users 13 and up to send and receive money—and lets parents monitor and manage transactions through Apple Cash Family.

Google Wallet stores similar items and works with Google Pay to make in-store and online payments. Previously, Google also offered family features like Purchase Requests, but those are no longer active in the U.S. as of mid-2024.

The structure is similar, but Apple provides a few more options for families managing younger users.

Payment Methods and Peer-to-Peer Transfers

Apple Pay supports peer-to-peer payments through Apple Cash, sent directly via iMessage. Once received, money sits in your Apple Cash card, ready to use or transfer to a bank account.

Google Pay also offered peer-to-peer transfers, but this feature has been discontinued in the U.S. While some international users still have access, it’s no longer a global option.

Both services support online and in-app purchases. At checkout, Apple users confirm payments with Face ID or Touch ID. Google users verify using a screen lock, biometric ID, or PIN.

Security You Can Trust

Security isn’t an extra, it’s standard.

Both Apple Pay and Google Pay use NFC and tokenisation to keep your card details safe. But how they handle your card data behind the scenes is very different.

Apple Pay:

- Uses a Device Account Number (DAN) stored on a secure chip.

- Transactions never reveal your real card number.

- Apple does not track your purchases.

Google Pay:

- Acts as an intermediary.

- Stores your card info on Google’s servers.

- Issues a virtual card number for every transaction.

- Google can access card data, but merchants can’t.

Both models prevent merchants from seeing your real card details. But only Apple has made a point of not collecting transaction data for its own use.

Transaction Costs

Neither Apple Pay nor Google Wallet charges users to make payments. Their business models are different:

- Apple Pay earns a small fee from the issuing bank

- Google Pay earns revenue through transaction fees to merchants and targeted ad services

There are no fees to the consumer. You just link your card, and you’re good to go.

Where They Work

Apple Pay is accepted in over 80 countries.

Google Pay supports transactions in more than 90 regions, depending on banking and regulatory approval.

Both are accepted at most retailers that support contactless payment.

Adoption is growing quickly. According to Digital Wallet Statistic by Finder, in 2024, around 4.3 billion people were using digital wallets globally—over half the world’s population. That number is expected to hit 68% by 2029.

Apple Pay alone had 640 million active users around the world, according to a report in Capital One Shopping.

These systems are no longer emerging. They are already part of how the world pays.

If you’re running physical or online checkout systems, both options integrate with major POS providers and payment gateways.

What Makes Each One Different?

If you’re trying to understand how Apple Pay and Google Pay stack up, here’s a quick breakdown:

Apple Pay vs Google Pay: Moving Forward

These payment systems aren’t trying to compete for your attention - they are built to work within specific device ecosystems. If you are using Apple or Android, each service gives you access to safe, fast, and modern ways to pay and manage your digital wallet.

Contactless payments are now a global standard. Knowing how they work -and where they differ - puts you in control of how you and your customers pay.

Start implementing Google Pay and Apple Pay into your payment strategy.

Get in touch with finera. to see how our platform supports secure, scalable payment solutions built for business.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Google Pay and Apple Pay both use NFC technology to enable secure, contactless payments. They function similarly at checkout, but Apple Pay only works on Apple devices, while Google Pay works on Android phones and Wear OS watches.

Yes. Both Apple Pay and Google Pay are accepted at most retailers with tap-to-pay terminals. If a store accepts contactless payments, it should work with both services.

The main difference is the ecosystem. Apple Pay is tied to Apple Wallet and exclusive to iOS devices, while Google Pay is designed for Android and integrates more with Google services, offering rewards and broader banking support.

Both Apple Pay and Google Pay are highly secure. They use tokenisation, encryption, and biometric authentication (Face ID, Touch ID, or fingerprint/lock screen on Android). Neither shares your actual card number with merchants.

You can’t use both on the same phone, since Apple Pay only works on iPhones and Google Pay only works on Android devices. However, if you own multiple devices, you can set up Apple Pay on your iPhone and Google Pay on your Android phone or smartwatch.

No, both Apple Pay and Google Pay are free to use. Your bank or card issuer may have standard transaction fees (like foreign transaction fees), but the payment services themselves don’t add extra charges.

Yes, both Apple Pay and Google Pay can be used for in-app purchases and online checkouts where their logos are displayed. Apple Pay often integrates directly into Safari on iOS and Mac, while Google Pay is supported in Chrome and Android apps.

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!