The Architecture of a Payment Gateway: The 8-Step Flow That Secures Your Revenue

Demystify the Payment Gateway. Explore the eight steps of the payment processing system in a guide.

For every online transaction, a secure, high-speed exchange of data occurs behind the scenes.

The payment gateway is the essential technology that processes customer details, links your checkout to the banking network and ultimately guarantees you receive payments.

But what exactly happens in the millisecond between a customer clicking 'Pay Now' and the approval notification appearing?

This guide breaks down the architecture of a payment gateway and explains the eight critical steps involved in every online payment. Understanding this payment processing system is vital for any merchant looking to future-proof their checkout stack, reduce friction and minimise declines.

Let's break down the anatomy of the technology that powers your global commerce.

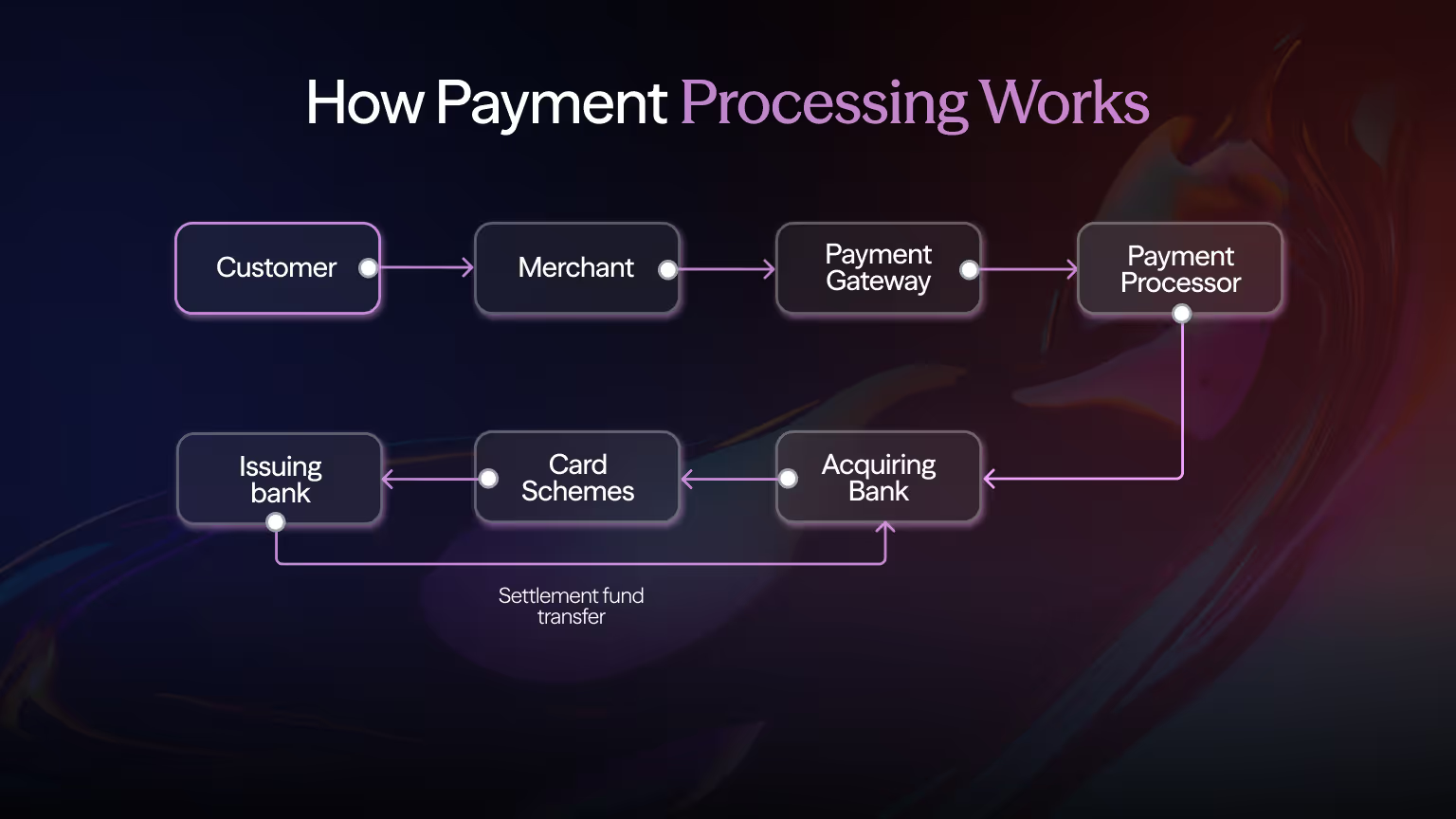

The Transaction Flow: The Eight Essential Steps

The entire process, from data entry to fund confirmation, typically takes under two seconds. For clarity, we can break this rapid exchange into four distinct phases:

Initiation, Authorisation, Clearing and Settlement.

Initiation Phase (Steps 1 & 2)

This phase begins with the customer and ends with the secure arrival of data at the Gateway.

- Data Capture: The customer enters their payment details (card number, expiry, CVV) on the merchant's checkout page.

- Encryption & Submission: The merchant's system securely encrypts the sensitive payment data (a critical step for PCI DSS compliance) and submits the request to the payment gateway. The gateway acts as the secure digital tunnel.

Authorisation Phase (Steps 3, 4, & 5)

This phase verifies the customer and confirms fund availability.

- The Request to the Acquirer: The payment gateway receives the encrypted transaction and routes it to the Acquirer (the merchant’s bank).

- Routing & Verification: The Acquirer forwards the request via the Card Network (e.g., Visa, Mastercard) to the Issuer (the customer's bank) via a payment processor. The Issuer verifies the card, checks for sufficient funds and runs fraud checks (like 3D Secure).

- Approval/Decline: The Issuer sends a final response (approved or declined) back through the Card Network to the Acquirer.

Clearing & Notification Phase (Step 6)

- Merchant Notification: The Acquirer passes the approval or decline status back to the payment gateway. The Gateway then sends a clean, actionable final status to the merchant’s website, completing the front-end checkout process for the customer.

Settlement Phase (Steps 7 & 8)

This phase involves the actual movement of money between banks.

- Batching & Funding Request: If the transaction was approved, it is now ready for clearing. The Acquirer formally requests the funds from the Issuer.

- Funds to Merchant: Once the Issuer releases the funds, the Acquirer deposits the money into the merchant’s bank account. The Processor is the service that batches the approved transactions and initiates the request for the actual funds from the Issuer Bank to begin the settlement process. This final transfer is the official Settlement of the transaction.

Understanding the Key Architectural Components of a Payment Gateway

To truly master your payment stack, you must understand the role of each player. These components are separate entities that the payment gateway is designed to connect seamlessly.

The Payment Gateway (The Secure Bridge)

The central piece of technology. Its primary functions are secure data encryption, routing to the appropriate Acquirer and returning a clear response. A modern gateway also integrates additional layers like risk management and real-time analytics.

The Acquirer Bank (The Merchant’s Partner)

This is the financial institution that holds the merchant's bank account and processes transactions on the merchant's behalf. They request the funds from the Issuer and handle the final settlement.

The Issuer Bank (The Customer’s Bank)

This institution issued the customer's card. They hold the final authority on the transaction, verifying the cardholder's identity and checking the account balance.

Payment Gateway vs Payment Processor

Are you confusing the term “payment gateway” with the “payment provider/processor”? You are not alone. While you often hear these terms used interchangeably, think of them as two different jobs in the payment journey.

The Payment Gateway is like the armoured postbox at your shop's checkout. Its job is front-facing, as it takes your customer's credit card information, locks it up securely (encryption) and quickly routes that order to the big banks. It's focused on security and data transfer.

The Payment Processor is the accountant at the bank. Its job is back-end by taking the order, checking the customer's account balance, officially recording the transaction and handling the actual moving of money between the customer's bank and your business account during settlement. It operates during the transaction process, yet it needs the payment gateway for communication.

In short, the Gateway secures the data, and the Processor moves the money.

Why Modern Commerce Needs Orchestration

While the anatomy above defines the basic function of a payment gateway, complexity arises when merchants pursue global growth.

A traditional, single Gateway often limits the merchant to a specific network of Acquirers. If that network performs poorly in a key international market (resulting in low approvals or high fees), the merchant lacks control and flexibility.

Payment orchestration platforms disrupt this model. They are a powerful layer above the traditional Gateway anatomy, allowing a merchant to integrate with one single API but access multiple Gateways, Acquirers and PSPs globally.

- Benefit 1: Higher Approvals: By using Smart Routing, the orchestration layer bypasses poor-performing Acquirers in real-time, routing transactions to the provider most likely to approve the payment in that region.

- Benefit 2: Flexibility: Merchants can easily add local Alternative Payment Methods (APMs), like Open Banking or local wallets, without having to rebuild their core checkout infrastructure, ensuring a future-proof checkout stack.

Read more about the differences between a payment gateway and payment orchestration.

Mastering Your Payment Stack with Payment Gateway

The payment gateway is the indispensable hub of your e-commerce operations. By understanding its eight-step anatomy, the secure process connecting the customer to the bank, you gain the power to diagnose issues and strategically optimise performance.

For merchants aiming for global resilience and maximum conversion, the shift is clear. Move from a static single-Gateway setup to a dynamic, multi-rail system powered by intelligent payment orchestration. This not only future-proofs your payment processing system but also ensures that every transaction has the highest possible chance of success.

Ready to transform your static Gateway into a high-performance orchestration engine?

Contact our team and see how finera. is redefining global payments.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!