Build vs Buy: Should You Build Your Own Payment Infrastructure?

Build or buy? Explore the trade-offs of owning vs outsourcing your payment stack and how to decide.

Optimising payment infrastructure is a strategic necessity, not just a technical choice, in the current global economy. For fintech platforms, marketplaces, and cross-border e-commerce businesses, how payments are handled can have a significant impact on profitability. That leads to one of the most debated questions in the industry today: build vs buy payment infrastructure.

At first glance, building your own payments stack seems to promise total control. Control over user experience, data flows, routing logic and interchange fees. But what often looks like a direct path to optimisation can quickly spiral into a costly and resource-heavy exercise.

This blog post will take a deep dive into the trade-offs, risks, and strategic considerations behind building versus buying a modern payment infrastructure, helping you make a data-driven decision.

The Appeal of Building In-House

The main advantage of building your own payment stack lies in complete ownership. You control every part of the stack, from integration with acquirers and schemes to fraud tooling and token vaults. This can be critical if payments are your product or your main differentiator in a crowded market.

Some of the theoretical benefits include:

- Custom routing logic tailored to your specific needs and geographies

- Direct interchange relationships that may reduce cost over time

- Full control of data flows and payment UX, improving branding and user experience

However, these advantages come with immense technical, financial and operational overhead.

The Hidden Costs of Building Your Payment Stack

Building a payment infrastructure from scratch is complex and expensive. It can take 12–18 months and several million dollars to build a scalable, compliant system.

Key challenges include:

- Compliance and security: You need to be PCI-DSS compliant and prepared to meet the evolving requirements of PSD2, GDPR and other regional regulations.

- Fraud prevention: Developing your own fraud detection engine and ongoing risk models demands a specialised team and constant iteration.

- Tokenisation: Storing and securing payment credentials calls for an in-house token vault and secure storage architecture.

- Integrations: Connecting to card schemes, alternative payment methods (APMs), open banking APIs, and local acquirers across regions involves extensive engineering and legal efforts.

- Redundancy and uptime: Guaranteeing 24/7 uptime with real-time failover and multi-acquirer fallback support requires a dedicated ops and SRE team.

- Reporting and reconciliation: Building reconciliation tools for multi-currency flows and across multiple providers is no small task.

Why More Businesses Are Buying or Partnering

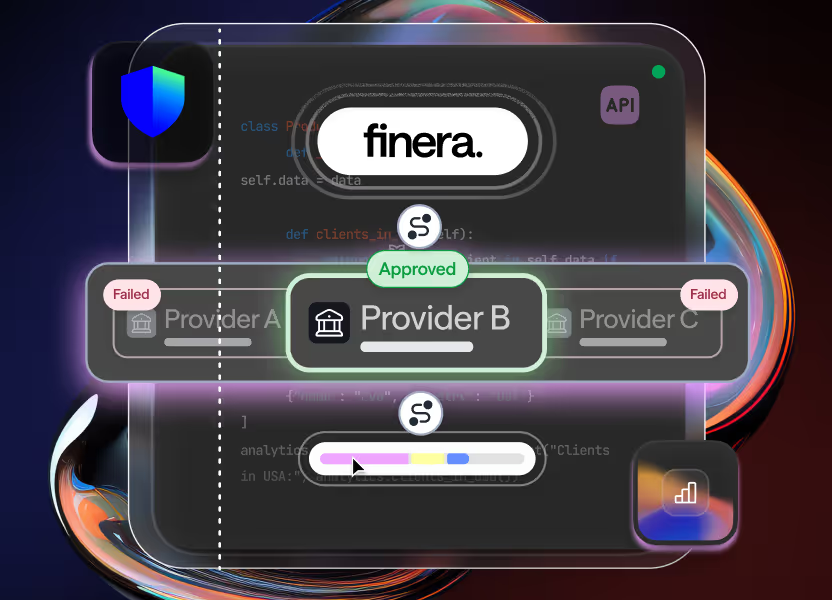

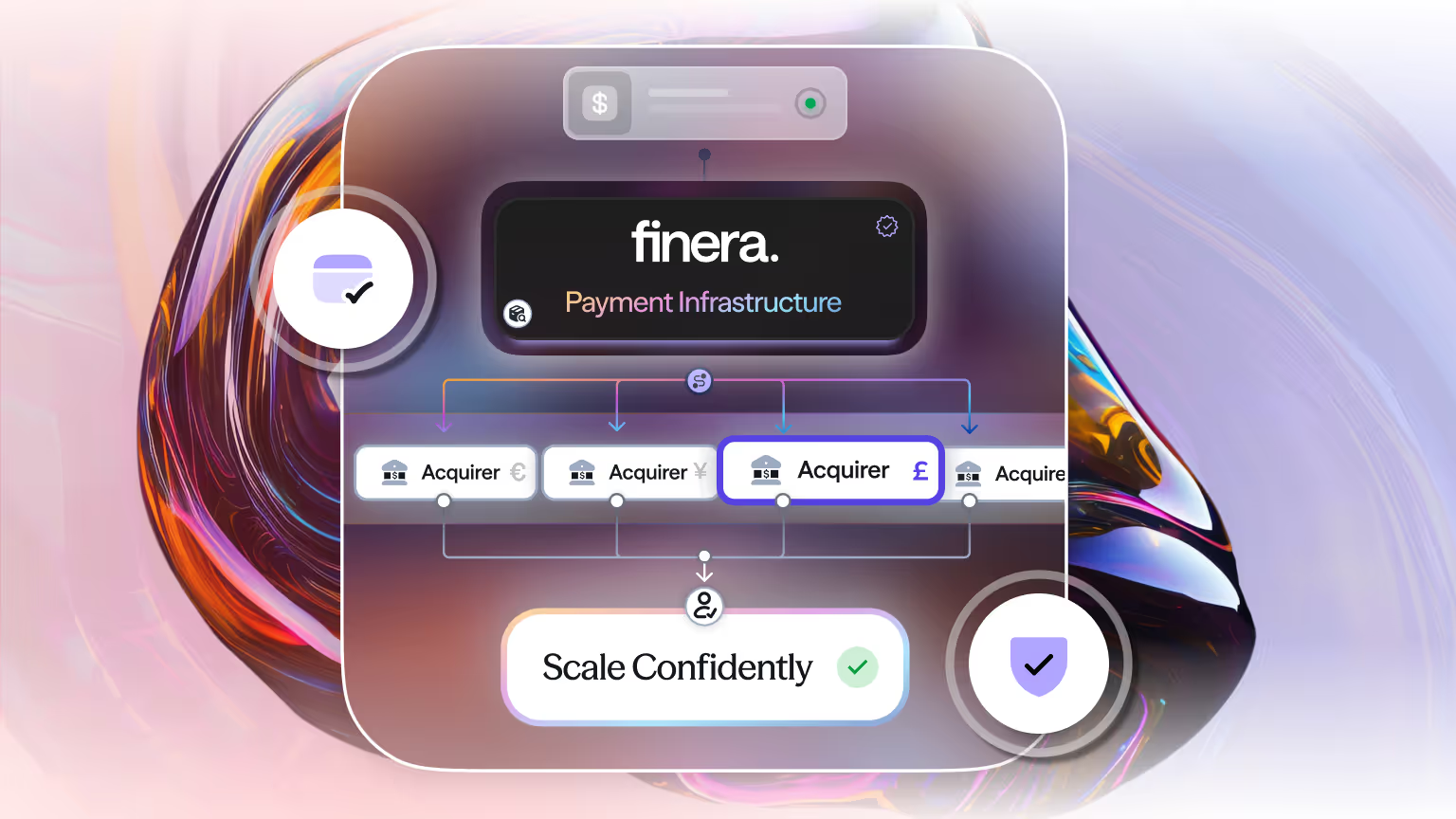

An increasing number of companies are turning to payment orchestration providers to manage the complexity of modern payments. Instead of building everything internally, they connect via a single API to a platform that offers the key components out of the box.

Payment orchestration platforms provide:

- Smart routing to improve approval rates by dynamically directing transactions

- Built-in fraud prevention using third-party risk engines and internal logic

- Multi-acquirer and APM support through one integration

- Real-time monitoring, analytics and reconciliation tools

With prebuilt infrastructure, onboarding is quicker, go-to-market times are faster, and internal teams can stay focused on core products rather than plumbing.

A Case for the Hybrid Approach

Some businesses choose a hybrid approach: they outsource the infrastructure to an orchestration partner but retain control over the decision-making logic or other critical layers.

This gives them the ability to:

- Customise routing rules per geography or customer segment

- Maintain proprietary fraud models or logic

- Leverage orchestration for scalability, redundancy and compliance

This is a flexible middle ground for businesses that want control without building everything from scratch.

The Risk of Getting It Wrong

Every failed transaction is lost revenue. Can your business afford friction in high-growth markets?

According to PaymentsJournal, global merchants are increasingly centralising their payment operations to reduce inefficiencies, manage costs and reduce failure rates.

Poor routing logic, downtime from a single point of failure, or the inability to support local payment methods can severely impact customer experience. In high-growth markets, that friction directly translates into churn, cart abandonment and lost revenue.

This is why the question, "Does my business need a payment orchestration platform?" is increasingly being asked in boardrooms and product teams alike. If you operate across borders, use multiple PSPs or want to optimise for both cost and approval rate, orchestration is no longer a nice-to-have. It’s a necessity.

What to Consider Before You Build

If you are still leaning toward building, make sure you have clarity on:

- Your volume forecast over the next 24 months

- Regional complexity (currencies, schemes, APMs, etc.)

- Internal engineering bandwidth

- Risk tolerance for downtime and regulatory changes

- How much of your stack needs to be proprietary to deliver customer value

Then compare that against the time-to-market, opportunity cost, and ongoing maintenance of a built solution.

Buying Lets You Focus on Growth, Not Infrastructure

Modern payment orchestration providers offer scalable infrastructure that meets today’s demands for speed, conversion and resilience. They invest in multi-currency support, smart routing, open banking integration and analytics tools so you don’t have to.

Instead of spending a year integrating acquirers, platforms can launch in weeks with embedded intelligence for routing, retries, fraud detection and reconciliation.

The result? Faster launches, better uptime, improved approval rates and a checkout experience designed for conversion.

Should You Build vs Buy Your Payment Infrastructure?

In the debate of build vs buy payment infrastructure, there’s no one-size-fits-all answer. But for most businesses, buying or partnering with an orchestration platform is the more practical, scalable and cost-effective choice.

If payments are not your core product, then building an in-house stack can become a distraction from your real business goals. Your business will achieve better results through quicker development when you select the right orchestration partner and direct resources toward customer experience improvement.

At finera., we help businesses simplify payments with payment orchestration, smart routing, multi-currency support and 24/7 customer service. From scaling internationally to optimising approval rates, our payment ecosystem is built to support your growth.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!