Open Banking and Its Role in Modern Payment Infrastructure

Discover the role of open banking in the modern payment infrastructure.

Remember when paying for something online meant scrambling for your credit card, meticulously typing out a 16-digit number, expiry date plus the CVV? It was a tedious process, fraught with the small anxieties of potential fraud and the slow-burning frustration of a declined transaction. For decades, this was the standard, a necessary friction in the digital world.

But the world of money is changing and it's happening quietly, right beneath the surface of our everyday transactions. The credit card is no longer the final word in digital payments.

This shift introduces open banking.

A paradigm shift that’s not just a new payment method but a complete overhaul of the plumbing that powers our financial lives. It's the engine running a silent revolution and it's fundamentally reshaping the very foundation of modern payment infrastructure.

So, what exactly is this powerful new force and how is it making our financial lives faster, cheaper and more secure?

Understanding the Limitations of Traditional Payments

Before we can appreciate the revolution, we have to understand the old guard. For most of the digital age, our payment system was dominated by a few major players like credit card networks, banks and a handful of digital wallet providers. This system, while functional, was built on a fragmented model of “walled gardens.” Each bank held its customers' data close and a fee-laden, multi-step process was required to move money.

Think about a standard card payment:

A transaction doesn't just go from your account to the merchant’s. It travels from the merchant's payment gateway, to their acquiring bank, to the card network (like Visa or Mastercard) and finally to your issuing bank. Each step adds layers of complexity, cost (known as interchange fees) and time. For merchants, these fees eat into their profits and for consumers, it's a clunky process with a lingering risk of fraud if card details are compromised. This system was ripe for disruption and open banking provided the perfect catalyst.

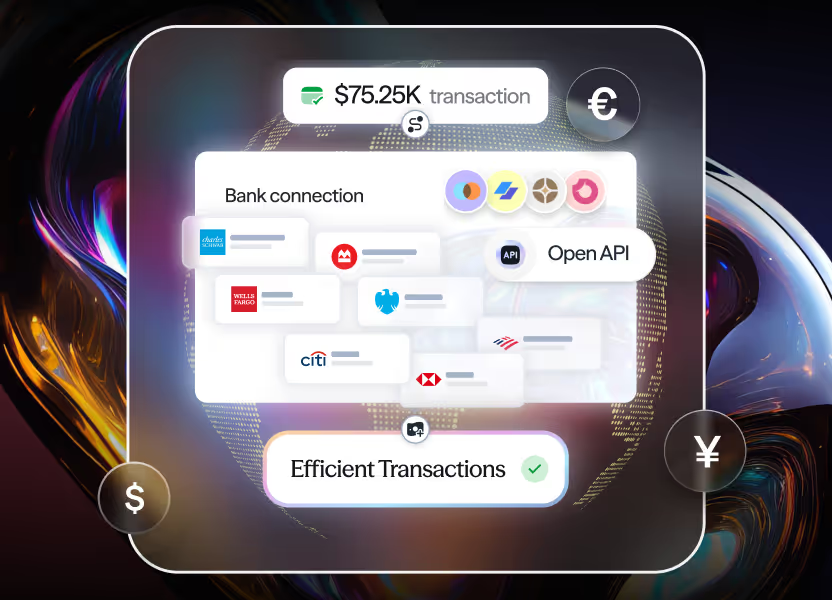

Open Banking and the Role of APIs in Finance

At its core, open banking is a secure way of sharing financial data with third-party providers (TPPs) through a technology called APIs (Application Programming Interfaces). Think of an API as a secure digital bridge that allows different computer systems to talk to each other. In the context of finance, it's the bridge between your bank and a trusted app or service.

The critical part of this is that it's all based on consumer consent. You are the one in control. You grant an app permission to access your financial data, whether to see your transactions or to initiate a payment on your behalf. This is a crucial shift from the old model, where banks acted as exclusive gatekeepers of your information.

This new ecosystem is primarily driven by two key services, which are mandated by regulations like the European Union's PSD2 (Payment Services Directive 2):

- Account Information Services (AIS): This allows third-party apps to access your account information (with your permission). This is the power behind popular personal finance management (PFM) apps that give you a holistic view of all your bank accounts in one place.

- Payment Initiation Services (PIS): This is the game-changer for payment infrastructure. It allows a third party to initiate a payment directly from your bank account to a merchant's account, all with your explicit consent.

How Open Banking Reshapes Modern Payment Infrastructure

With Payment Initiation Services at the helm, open banking is not just an alternative, it’s a superior way to pay. It fundamentally rewires the payment process, creating a more direct and efficient flow of funds.

Direct and Cost-Effective Payments

The most immediate benefit is cost-effectiveness. By using PIS, a merchant can bypass the costly card networks entirely. There are no interchange fees, no acquiring fees, and often lower processing costs. This makes open banking payments significantly cheaper than card payments, a huge win for businesses, especially small and medium-sized enterprises (SMEs). Merchants can pass these savings on to consumers or reinvest them back into their business. This also makes the process more transparent, as there's a clear, direct transaction from sender to receiver.

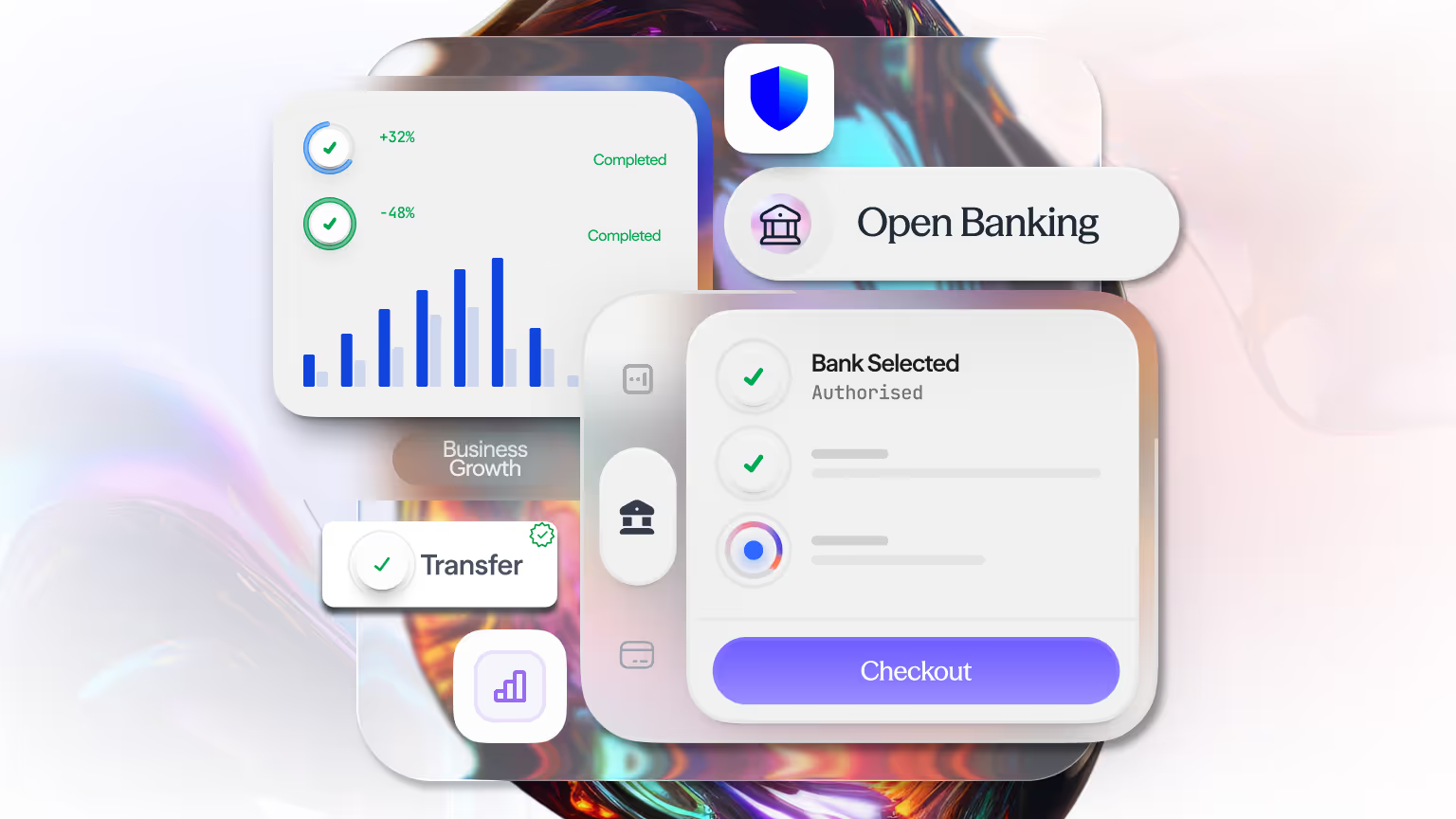

Enhanced Security and Fraud Prevention

In the traditional model, a consumer's card details are entered on a merchant's website, then transferred through multiple parties, creating multiple points of vulnerability. With an open banking payment, you are redirected to your bank’s secure portal to authenticate the transaction. The merchant never sees or stores your sensitive financial information. The payment is authenticated using your bank's strong security measures, such as biometrics or two-factor authentication. This dramatically reduces the risk of fraud and gives both the consumer and the merchant greater peace of mind.

Speed and Efficiency in Digital Payments

Unlike traditional bank transfers that can take days to clear, open banking payments are often settled in near real-time. This instant flow of funds is a massive advantage for businesses, improving cash flow and accelerating services. Imagine paying for a service and having access to it instantly or a business receiving a payment without the frustrating wait time. This speed also powers innovation in areas like B2B invoicing and cross-border payments, where delays can be extremely costly.

The Future of E-commerce and Mobile Payments

Open banking payments offer a streamlined and intuitive user experience. There's no fumbling for a wallet or remembering a password. Instead, you click a "Pay by Bank" button, are securely redirected to your bank app, authenticate the payment and you're done. This is particularly appealing for mobile commerce and digital payments, where a quick and frictionless checkout process is key to converting customers.

Beyond Payments: Open Banking’s Impact on Financial Services

While its role in modern payment infrastructure is the most visible benefit, open banking’s reach extends far beyond. The ability to securely share financial data has unlocked a wave of fintech innovation.

- Enhanced Financial Management: Apps that use Account Information Services can aggregate all of your accounts, credit cards and investments into a single dashboard. This gives you a clear, holistic view of your finances, helping you budget more effectively and achieve your financial goals.

- Improved Lending and Credit Scoring: Lenders can now, with your consent, access a real-time, comprehensive view of your income, spending habits and existing debt. This provides a much richer and more accurate picture than a traditional credit score, leading to fairer and more personalised loan offers. It can even help people with thin credit files get access to credit they might have been denied otherwise.

- Smarter Financial Services: open banking data enables new services that were previously impossible. Think of an app that analyses your spending to find subscriptions you can cancel or a tool that helps you automatically find and switch to a better-value savings account or utility provider.

The Future of Payments: Challenges and Opportunities

Despite its immense promise, the widespread adoption of open banking faces challenges. Consumer trust is a primary hurdle, convincing people to share their financial data, even with their consent, requires a strong message about security and benefit. Global standardisation and regulatory alignment are also ongoing processes that will determine the pace of its worldwide adoption.

However, the trajectory is clear. As more consumers experience the speed, security and convenience of open banking-powered payments and financial services, it will become the new standard. It's not just about a new way to pay but about a new, open and consumer-centric financial ecosystem. The traditional walls are coming down and in their place, a faster, more intelligent and more connected payment infrastructure is emerging.

Ready to integrate open banking and start maximising your revenue? Don't let your payment infrastructure hold you back from a future of lower costs and higher conversions. Get in touch with our team today and find out how finera. can transform your payment infrastructure.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

.avif)

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!