Why Local Acquiring Improves Transaction Approval and Payment Performance Across Europe

Explore why local acquiring can improve approval rates across European markets.

Businesses objective is to provide their customers with flawless payment systems and experiences which operate without any location-based restrictions.

Businesses that operate in Europe should select local acquiring systems because these solutions prove to be smart choices. The system produces major changes which improve transaction approval percentages while it creates a more efficient checkout experience and reduces operational problems for all parties involved.

What does local acquiring mean? It simply means processing card payments and other payment types through banks or processors that are based in the same country or market as the customer. The issuing banks will approve transactions which go through domestic acquirers instead of cross-border systems when iGaming and e-commerce transactions occur.

Merchants need to understand that their local ties become vital because European payment markets have evolved into intense competition, while users demand flawless service delivery.

Europe’s Unique Payments Landscape

Europe is often discussed as if it were a single, homogeneous market. However, the reality is quite different. While initiatives like SEPA (Single Euro Payments Area) and PSD2 (Payment Services Directive 2) harmonise parts of the regulatory framework, the region remains a complex patchwork of national banking systems, consumer behaviours and preferred payment methods.

In one European market, customers may default to local debit cards and in another, they may prefer digital wallets or real-time bank transfers. Simultaneously, issuers apply risk and authentication rules that reflect domestic expectations.

When a French consumer’s transaction is processed through a non-French acquirer, for example, issuing banks may view that activity as cross-border, triggering additional checks or declines. For merchants, this can translate into higher decline rates, longer checkout times and a poorer user experience.

Because Europe’s infrastructure varies so widely, local acquiring solutions help align transaction processing with consumer and issuer expectations. This alignment directly influences the three pillars of checkout performance: reliability, speed and trust.

Local Acquiring and Higher Approval Rates

The core metric on which payment performance depends exists in the approval rate because it shows the percentage of transaction attempts that can result in successful completion. The approval process depends on various elements, yet routing stands out as a major determining factor. The issuing banks treat domestic acquirer transactions which follow domestic acquisition routes as they would handle their regular business operations. The system identifies familiar traffic, which leads to reduced security alerts that block authorised users from accessing their accounts.

Local acquirers also have a deeper understanding of domestic authentication flows, network preferences, and risk profiles. This knowledge allows them to apply Strong Customer Authentication (SCA) and other compliance requirements in ways that feel natural to local customers, reducing friction without sacrificing regulatory alignment.

As a result, merchants using local acquiring can see improved approval rates across markets. Higher approval rates lead to businesses maximising their revenue potential during checkout while customers complete their purchases without leaving their carts behind and customers avoid multiple payment attempts or method changes.

The advantages of higher approval rates become particularly important for businesses operating in high-volume markets, which include e-commerce, digital services and iGaming.

Performance and Technical Benefits

Transaction performance isn’t only about approval rates, it also speaks to the entire payment journey. Transactions processed through local acquiring infrastructure often experience lower latency because they leverage domestic networks with fewer intermediaries. This can shorten authorisation times and reduce the number of technical failures that sometimes occur when transactions traverse multiple international hops.

The system enables faster payment processing, which leads to checkout systems that respond more quickly to user interactions. Customers today want to receive immediate responses because they use mobile devices, which make up an increasing portion of digital commerce.

The checkout process becomes broken when payments fail to process or time out because the payment system fails to complete its intended function. Merchants who operate payment systems within their own community can create an unbroken payment path, which starts with customer intentions until the final payment confirmation.

Local acquiring functions as a straightforward solution, which enables businesses to manage their settlement and reconciliation processes. Domestic acquiring partners offer reporting and settlement services, which use local currency to simplify operations while helping finance teams achieve better reconciliation of their activities.

Enhancing the Customer Experience

From the customer’s perspective, the benefits of local acquiring show up as fewer interruptions and more consistent checkout flows. Customers do not care whether a transaction was processed via a local, regional or global provider, they only care that it works smoothly and securely.

Local acquiring reduces the risk of unexpected payment declines, which also helps prevent authentication procedures from becoming confusing and stops payment authorisations from taking too long. This can damage customer trust during their checkout process. A customer who receives approval on their initial attempt will view the outcome as an easy process. People base their trust in digital platforms on their ability to work properly because they want to experience smooth online interactions, which lead to customer loyalty and repeated business.

Local acquiring creates better performance across different markets, which leads customers to finish their purchases, while they also come back for future purchases and they will suggest the merchant platform to their friends. Merchants who operate in different countries need to find unique ways to stand out from their competitors because this strategy will help them compete effectively in international markets.

The Role of Local Payment Methods

Local acquirers also make it easier to integrate and manage local payment methods (LPMs) or alternative payment methods (APMs), which remain an important part of Europe’s payment mix.

In some markets, domestic debit systems, bank transfers and wallets are deeply embedded into consumer behaviour. A local acquirer is often better positioned to support these methods seamlessly alongside global cards.

Rather than treating Europe as a single block of translated payment options, merchants can present payment choices that genuinely reflect local preferences. This context-aware kind of checkout optimisation can help improve conversion and reinforce customer confidence.

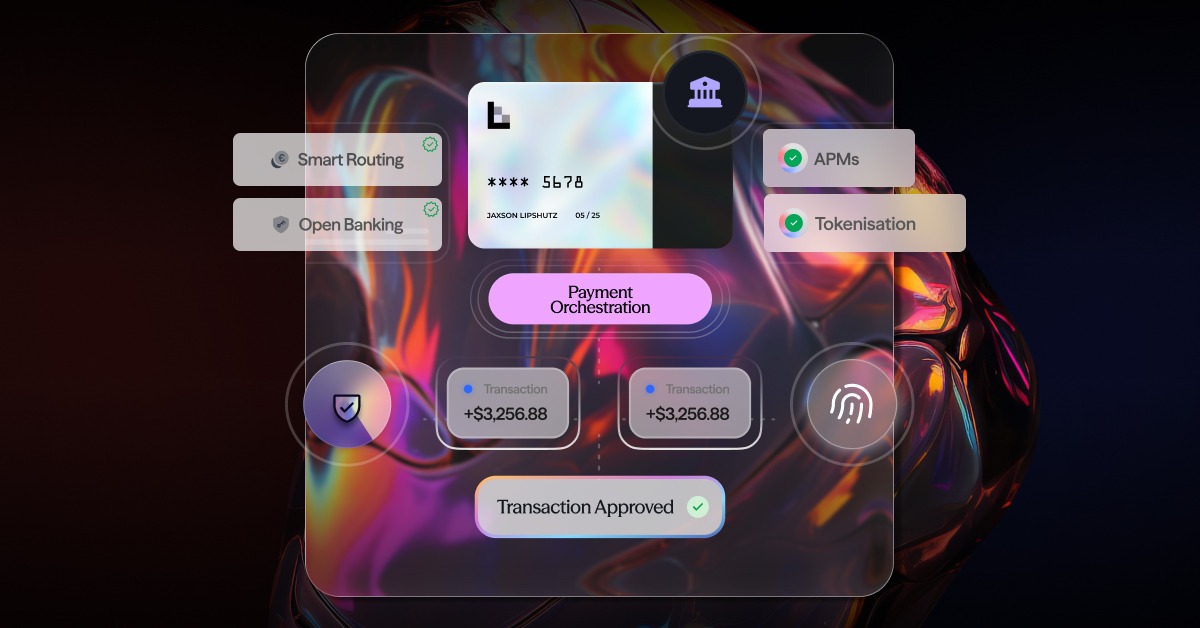

Boosting Approval Rates with Payment Orchestration

While local acquiring delivers technical and commercial advantages, integrating and managing multiple local acquiring partners can be operationally complex. This is where payment orchestration becomes a strategic enabler.

A payment orchestration layer allows merchants to connect to multiple domestic acquirers and manage transaction routing intelligently. Orchestration abstracts the complexity of direct integrations, allowing merchants to:

- Route transactions based on geography, currency or performance.

- Monitor approval rates and handle exceptions centrally.

- Adjust routing strategies without rebuilding checkout infrastructure.

- Present a unified reporting and reconciliation experience.

In essence, payment orchestration makes local acquiring practical and scalable. Rather than maintaining siloed integrations for each market, merchants can optimise routing logic dynamically and improve performance across Europe from a single platform.

The Strategic Case for Local Expertise

Multiple payment systems across different markets will continue to operate throughout Europe for the upcoming years. The banking system, together with customer habits and regulatory frameworks maintain distinct operational systems which do not form a unified structure. Merchants who view Europe as separate but linked markets can create payment systems which match actual consumer purchasing patterns.

Local acquiring, supported by payment orchestration, helps merchants scale sustainably across borders. The system improves approval rates while it decreases checkout obstacles and it meets compliance requirements and provides users with a better experience.

Local Acquiring as a Cornerstone of European Payment Strategy

Local acquiring is becoming a strategic necessity for merchants who want to deliver reliable payment performance across Europe. Aligning transactions with domestic infrastructure can significantly improve approval rates, reduce declines and help offer a smoother checkout for customers.

Supported by payment orchestration, local acquiring enables a scalable, resilient payment infrastructure that adapts to the demands of diverse European markets. For merchants seeking consistent performance and long-term growth, this combination offers a practical path forward.

Find out how local expertise drives global success. Talk to the finera. team to explore how local acquiring and payment orchestration can strengthen your European payment strategy.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!