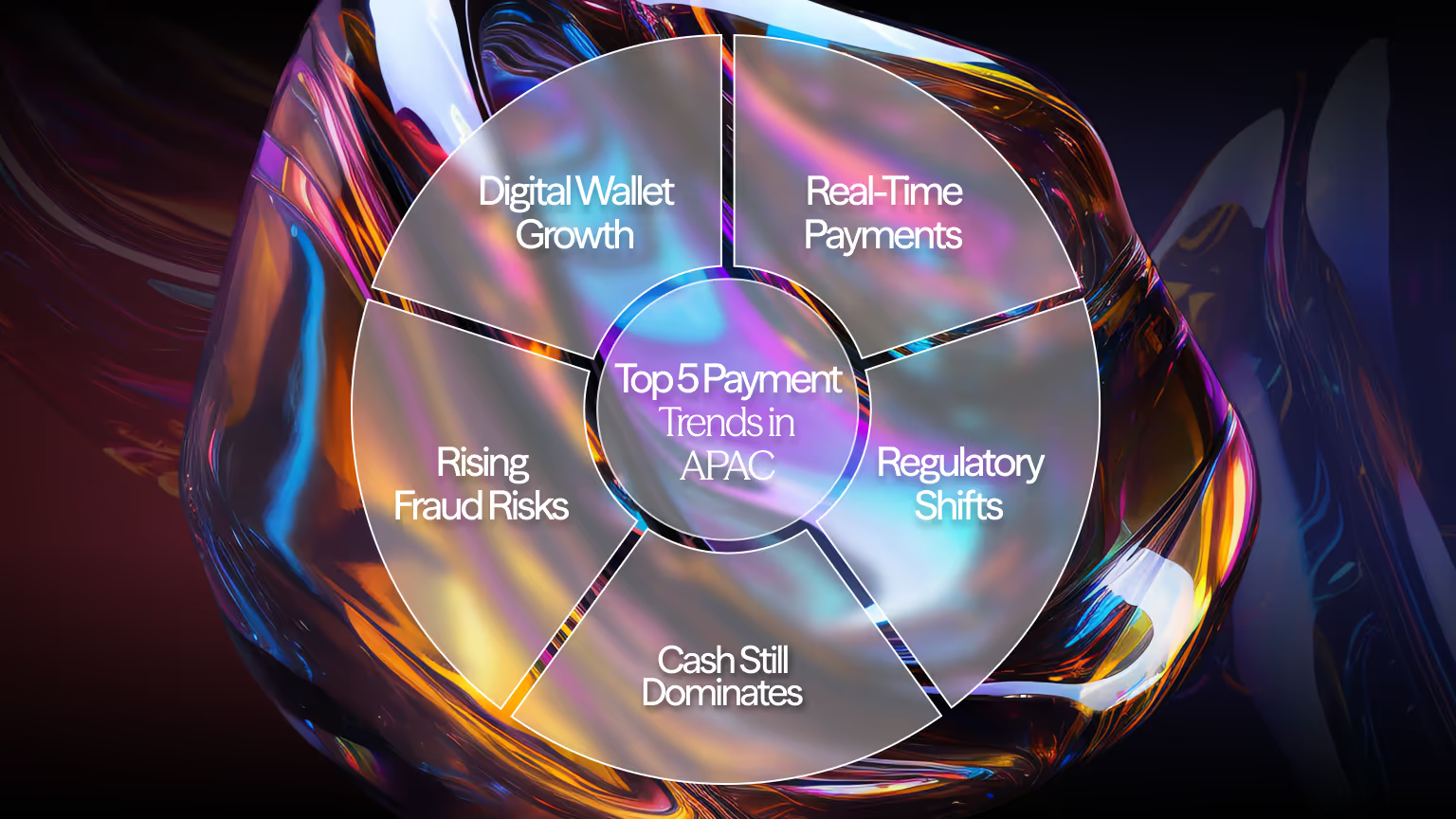

Top 5 Payment Trends in APAC (2025)

APAC payments 2025: Wallets, UPI, Crypto and RTP reshape global commerce.

If you want to see where payments are headed, look east. Right now in 2025, the Asia-Pacific region (APAC) is setting the pace for the rest of the world.

In China, cash is practically obsolete. In India, UPI has turned instant bank transfers into a daily habit for nearly half a billion people. And in Vietnam, QR payments are surging month after month, quickly replacing wallets in people’s pockets.

Across the region, regulators, banks and fintechs are moving fast. Singapore is laying down rules for stablecoins, Australia is rolling real-time payments into almost every retail bank account and Japan is drawing global players eager to break into its market.

For merchants, this makes APAC both a massive opportunity and a complex challenge. Payment preferences are hyper-local, customer expectations are sky-high, and what works in one country can completely fail in another. To succeed, businesses need to keep up with the latest payment trends in APAC and, more importantly, know how to act on them.

Key Payment Challenges in the Asia-Pacific Market in 2025

APAC may be the world’s most exciting payments region, but it’s not without growing pains. For every innovation that takes off, there is a hurdle that merchants and providers need to solve.

Fragmentation is among the most significant obstacles. APAC does not have a unified payments system like the US or the EU. Every nation has its own laws, customs and rules. It is frequently necessary for a merchant to rebuild their payment stack virtually from scratch when they expand from Singapore to Indonesia or Vietnam.

Cross-border costs are another sticking point. While local real-time payments (like India’s UPI or Australia’s NPP) are fast and cheap, sending money between countries can still be slow and expensive. That’s a big problem for e-commerce platforms and travel companies trying to serve customers across borders.

Then there’s the issue of cash dependency.

Even though digital adoption is skyrocketing, cash still dominates in certain markets. India’s 60% cash-based consumption is the most visible example. Merchants must balance investing in the future with meeting customers where they are today.

Finally, the risk of fraud keeps increasing. Bad actors are coming up with new strategies to take advantage of cross-border vulnerabilities or inadequate authentication as more people purchase and make payments online. Regulators like the Monetary Authority of Singapore and the Reserve Bank of India are responding with tighter controls, but merchants often find compliance costly and complicated.

The takeaway? APAC payments are developing more quickly than any other region, yet navigating the area calls for adaptability, local expertise and the appropriate technology.

Payment Trends and Country Snapshots in APAC (2025)

While the Asia-Pacific payments market is diverse, a few common themes emerge, like rapid digitalisation, regulatory shifts and heavy consumer demand for faster, cheaper and more localised options. PwC's payment insights indicate that real-time payments for value-added use cases are growing, lending models and laws are changing, innovations in efficient cross-border transfers are becoming more common, the adoption of digital currencies is growing fast and new digital banks are developing.

But if you look more closely at each country, you can see that these trends show up in different ways.

Australia: Diverse Payment Mix with Strong BNPL Adoption

The payment market in Australia is a reflection of both customer choice and innovation. Digital wallets now make up 39% of eCommerce transactions, according to data from World Pay GPR 2025. However, what truly sticks out is the strength of BNPL, which has one of the greatest adoption rates in the world at 15%. With credit at 19% and debit at 20%, cards continue to be important, indicating that Australians continue to rely on both new and conventional rails. With only 2% of transactions being conducted online, cash has essentially vanished. This mix means that in order to maximise conversion, retailers' checkout tactics need to strike a balance between more modern digital techniques and well-known card choices.

China: Digital Wallets Dominate Online Spending

China remains the undisputed global leader in wallet adoption. Digital wallets make up 84% of all e-commerce payments, dwarfing credit cards (5%) and debit cards (4%). Bank transfers (2%) and BNPL (4%) are niche compared to the scale of wallets like Alipay and WeChat Pay. Cash is practically irrelevant online, with less than 1% of usage. For merchants entering China, success depends on integrating local wallet ecosystems rather than relying on international card networks.

Hong Kong: Balancing Wallets and Bank Transfers

Hong Kong’s e-commerce payments are defined by a more balanced spread compared to mainland China. Digital wallets represent 36%, while account-to-account (A2A) transfers hold 15%. Credit card usage is still notable at 33%, but BNPL adoption remains relatively low at just 1%.

This mix demonstrates that in a market that connects the East and the West, bank-based payments and cards remain essential even as wallets gain traction. Both traditional banking habits and contemporary wallet options must be accommodated by merchants growing here.

Japan: Card Culture Still Dominates

Japan is a unique case in APAC. While digital wallets account for 25% of e-commerce transactions, cards remain the king of the country. Credit cards make up 55% and debit cards add another 4%, making Japan one of the most card-reliant countries in the region. Bank transfers (6%) and BNPL (2%) exist but remain small. Crypto and cash barely register. For international merchants, this highlights that Japan’s digital transformation is slower compared to neighbours like China or Korea. Adapting to a strong card culture while gradually introducing wallets and A2A options is the pragmatic approach.

Singapore: Stablecoins in the Spotlight

In Singapore, regulators are moving fast to shape the future. The Monetary Authority of Singapore (MAS) has clarified its framework for stablecoins, setting the stage for innovation while keeping risks in check. This makes Singapore one of the most progressive hubs for blockchain-based payments and a test bed for how regulated stablecoins could coexist with traditional rails.

Philippines: Digital Payments Go Mainstream

The Philippines is tackling one of the biggest barriers to adoption: fees. The country’s central bank is actively pushing for wider digital payment usage by eliminating transaction fees, making wallets and bank transfers far more attractive for consumers and merchants alike, according to Payments & Commerce Intelligence. This is a huge step in a market where cash has long dominated.

India: UPI’s Unstoppable Rise

India’s Unified Payments Interface (UPI) continues to dominate, with more than 450 million users by the end of 2024. Yet, there’s still huge room for growth: 60% of India’s consumption is still cash-based and UPI is reaching only half of the country’s internet users (Payments & Commerce Intelligence, 2025).

Vietnam: QR and NFC Growth at Record Pace

Vietnam’s digital payments are exploding. The use of digital wallets is expanding significantly, now accounting for 41% of all e-commerce purchases. QR payments are growing by an average of 6% every month, NFC payments are also climbing 6% monthly and Apple Pay alone is expanding by 15% per month. That level of growth points to a consumer base eager for mobile-first solutions and a market that’s quickly catching up with its more digitally mature neighbours.

South Korea: A Mobile-First Payments Powerhouse

South Korea is one of the most advanced digital payments markets in APAC. Wallet adoption is extremely high, driven by super-apps and mobile-first platforms like Kakao Pay, Naver Pay, and Toss. BNPL is gaining traction, particularly with younger consumers, while crypto payments are also carving out a niche. Yet, cards remain deeply entrenched, reflecting South Korea’s balance between cutting-edge innovation and established rails. For merchants, success here means integrating both mainstream card schemes and local wallet ecosystems.

Indonesia: Scale Meets Fragmentation

With over 270 million people, Indonesia is the fourth most populous country in the world and a fast-growing eCommerce giant. Payments here are defined by diversity: bank transfers and e-wallets (GoPay, OVO, Dana) dominate online transactions, while cash-on-delivery still lingers in rural areas. This fragmentation makes orchestration particularly valuable, helping merchants streamline checkout options while covering both urban wallet users and cash-dependent consumers.

Malaysia: QR Standardisation Leads the Way

Malaysia has embraced digitalisation, with the DuitNow QR standard emerging as the backbone of instant payments across banks and wallets. This move towards interoperability has accelerated wallet adoption, making digital payments far more accessible. At the same time, Malaysia’s role as a cross-border commerce hub in Southeast Asia means merchants must be prepared for both local wallet integrations and regional settlement demands.

Thailand: QR Payments on the Rise

Thailand’s payments market mirrors Vietnam in many ways, with QR-based transactions booming thanks to the government-backed PromptPay system. Adoption is widespread among both consumers and merchants, making QR codes a default option for many transactions. For cross-border merchants, local wallet compatibility is essential, as cards are less dominant compared to QR and A2A (account-to-account) methods.

Taiwan: Cards Still Strong But Wallets Growing

Taiwan remains a card-heavy market, with credit and debit usage still strong in e-commerce. However, digital wallets are quickly gaining ground, supported by a tech-savvy population and government encouragement of digital payments. For now, merchants cannot ignore cards in Taiwan but planning for increased wallet adoption will be key to future-proofing checkout strategies.

How Payment Orchestration Supports APAC Growth

To overcome key payment issues, merchants are increasingly turning to payment orchestration platforms. Businesses can use orchestration with a single integration to:

- Access multiple PSPs and local acquirers without separate contracts

- Use smart routing to boost approval rates and reduce failures

- Onboard local APMs quickly, from UPI to GCash

- Consolidate reporting and reconciliation across markets

- Support multi-currency pricing, improving transparency for customers

For merchants looking to expand into APAC, payment orchestration can be the key to achieving consistent cross-border success and avoiding high abandonment rates.

APAC Sets the Pace for Global Payments

The Asia-Pacific region is not merely adapting to changes in payment trends but it is actively leading the transformation. From UPI’s global reach and Singapore’s stablecoin clarity to Vietnam’s QR boom and Australia’s RTP expansion, APAC is leading the future of payments.

Merchants that want to thrive must embrace local payment methods, smart routing and orchestration to reduce friction, lower costs and increase approvals.

At finera. we understand the complexities of the APAC market. That’s why we offer payment orchestration, local integrations, a non-custodial crypto processing solution and 24/7 support to help your business expand seamlessly.

Contact our team today to simplify your APAC payments.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!