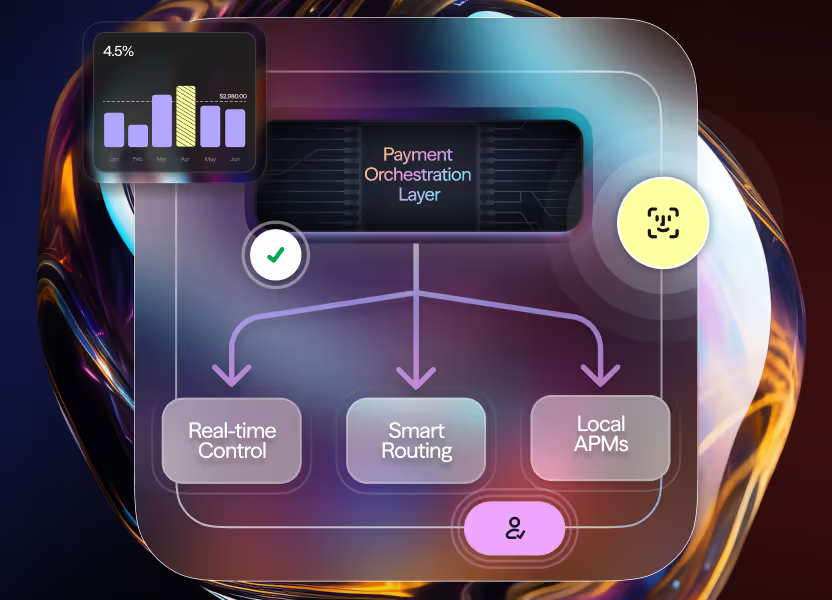

Single Point of Integration in Payment Orchestration

One API for European payments: smart routing, unified analytics & simpler PSD3/DORA compliance.

European merchants and platform operators are running into the same wall in 2026. Payment stacks that started simple have turned into a maintenance problem. Direct integrations with PSPs, acquirers, gateways, APMs and fraud tools pile up. Each one brings its own API quirks, its own compliance mapping, its own outage pattern. The result is slower launches, fragmented reporting and a growing list of things that can break at 3am on a Saturday.

A single point of integration flips that problem. The merchant connects once to an orchestration layer, and the payment orchestration layer handles the fan-out to cards, open banking, local APMs, payouts and fraud engines. The merchant stops being the integration team.

This is not a theoretical shift. Operators moving to orchestration are reporting faster market entry and cleaner analytics, and they are doing it without ripping out their stack every time PSD3 drops a new requirement or a new local APM becomes table stakes in a given country.

What follows is a practical look at what a single point of integration actually does for a European business, how it lines up with UK and EU rules in their current 2026 state, and where operators are seeing the numbers move.

Key Takeaways

- One API connection can stand in for multiple direct PSP integrations, which cuts engineering maintenance and shortens market entry from months to days.

- Dynamic routing has been observed to improve authorisation rates, with the exact uplift depending on traffic mix, issuer behaviour and configuration.

- Centralised data and tokenisation help merchants meet FCA Consumer Duty, DORA and the incoming PSD3 regime while keeping ownership of their payment analytics.

- A unified dashboard makes chargeback evidence, reconciliation and first-party misuse monitoring easier to run. The MRC 2026 Global eCommerce Payments and Fraud Report noted 64% of merchants saw first-party misuse rising.

- SEPA Instant, provider-agnostic network tokenisation and early agentic AI commerce protocols can be picked up through the same integration, without new engineering cycles.

- Results are configuration-dependent, but the move away from multi-integration stacks has been linked to total cost of ownership reductions of up to 30% for many mid to large-size operators.

Why Legacy Payment Stacks Create Friction for European Operators

The Hidden Costs of Multiple Direct Integrations

The old playbook for expansion was to build a direct API connection to each acquirer, gateway and APM. Every PSP release, every SCA rule change, every ISO 20022 migration then became a separate piece of work across the stack.

Teams ended up maintaining integrations instead of shipping products. That drag shows up most clearly in markets like the UK, Ireland and Malta, where shoppers now expect local card acquiring and familiar APMs at checkout.

When Gateways and Aggregators Fall Short

A single gateway or aggregator makes the first connection easy. It also creates new problems. Vendor lock-in, patchy APM coverage, and one point of failure during an outage.

If the provider does not support a key local method like iDEAL or Blik, the merchant has to bolt in another integration outside the main flow, which is exactly what the gateway was supposed to prevent.

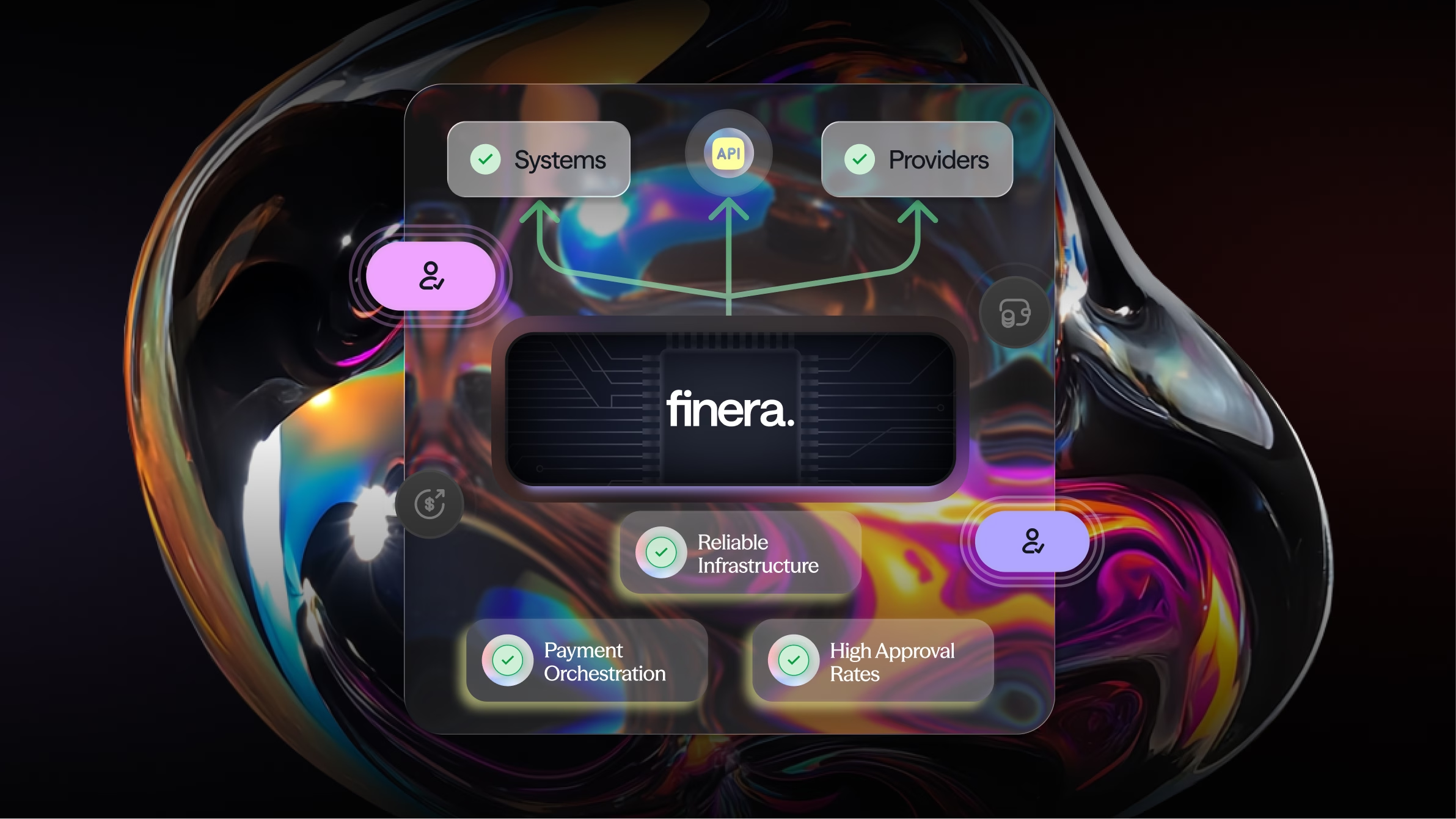

Orchestration sits a layer above. The merchant keeps one clean API and gets access to multiple independent providers behind it.

What a Single Point of Integration Actually Delivers

One API, Many Rails

The orchestration layer is the single entry point to cards, open banking, APMs, fraud engines and payout rails. The merchant sends one payload.

The platform handles routing, formatting and compliance checks behind it. Adding a new market usually means enabling a new route rather than writing a new integration.

How Orchestration Sits Above the Payment Layer

It works like a smart switchboard. Transaction data goes into the orchestrator, which looks at BIN, issuer, geography, cost and real-time risk score, and then directs the payment to the best available processor.

Soft or technical declines can be retried on a different route in milliseconds. The merchant sees one consistent response format and one dashboard covering everything.

UK and EU Regulatory Pressure That Makes Orchestration Strategic in 2026

FCA Consumer Duty and Operational Resilience (UK)

The FCA’s March 2026 Regulatory Priorities report is still leaning hard on effective Consumer Duty implementation, transparent customer outcomes and safeguarding of client funds.

A single integration point helps operators standardise checkout journeys and pull unified data for demonstrating fair outcomes across every payment route.

The PRA’s operational resilience expectations are also easier to evidence when failover and continuity live inside the routing logic rather than in a runbook.

DORA, the PSD3 Transition and AMLA (EU, with UK Divergence)

DORA has been in full supervisory mode since January 2025, and ICT third-party risk management is still the priority that regulators keep coming back to. Payment Services Regulation and the accompanying PSD3 are expected to finalise in H1 2026 with application from 2027. Re-licensing, stronger SCA rules and clearer open-banking access are the headline items.

Orchestration platforms can centralise SCA logic, dynamic exemptions and incident reporting, which makes it easier for merchants to evidence compliance without running a separate rule set per acquirer.

AMLA’s growing cross-border oversight benefits from unified transaction monitoring across fiat rails and, where relevant, crypto rails. None of this guarantees compliance on its own, but it takes a lot of plumbing out of the problem.

Real-World Performance Gains Operators Are Seeing

Smart Routing and Approval-Rate Impact

Intelligent routing scores each transaction in milliseconds and picks the processor statistically most likely to approve it. Soft declines fail over automatically without adding friction for the customer.

European implementations have reported authorisation uplifts of 2-5 percentage points when routing logic accounts for cost, performance and geography. The ceiling depends on vertical, issuer mix and traffic profile.

Centralised Fraud, Chargeback and Reconciliation Management

The MRC 2026 report flagged that 64% of merchants saw first-party misuse rising, with many also reporting more refund abuse. A unified orchestration dashboard pulls risk scores, 3DS data, settlement files and dispute evidence from every route into one place.

Operators can watch chargeback ratios by acquirer, throttle risky traffic automatically and put representation packages together faster. Reconciliation shifts from spreadsheet work to near real-time visibility, which is the bigger operational win in most programmes.

2026-2027 Technology That a Single Integration Unlocks

Network Tokenisation, Real-Time Payments and Agentic AI Readiness

Provider-agnostic tokenisation lets merchants swap sensitive card data for network tokens that move securely across any connected acquirer. SEPA Instant is now mandatory across much of the euro area, and orchestration centralises the fraud checks that irreversible instant settlement makes non-negotiable.

Early agentic commerce protocols (machine-to-machine payments) can also be picked up through the same single API, which avoids backend rewrites as the standards mature in 2027.

What This Means for Merchants and Operators in 2026

Payment infrastructure is no longer a back-office utility. It is a competitive lever and a regulatory one. A single point of integration through orchestration gives European operators control over routing, data and resilience while reducing engineering overhead and compliance friction. None of the gains are automatic.

They depend on configuration, route coverage and ongoing tuning. The pattern across operators who have done the work is reasonably consistent, though: quicker market entry, faster response to regulatory shifts like PSD3 and DORA, and higher approval rates with lower operational risk.

For iGaming, travel, SaaS and cross-border e-commerce, this is becoming the practical way to scale across the UK, EU and secondary markets such as Cyprus, Malta, Ireland and Gibraltar. As 2027 brings PSD3 into force and open banking deepens, the operators already running on a modern single-integration foundation will have a lot less retrofitting to do.

FAQs

What is the difference between a payment orchestration platform and a traditional gateway?

A gateway typically connects to one or a small set of acquirers, which leaves a single point of failure. Orchestration sits above multiple gateways and acquirers, with one API for the merchant plus intelligent routing, failover and unified analytics on top.

How quickly can orchestration improve time-to-market in new European countries?

New local APMs or acquirers are commonly onboarded in days rather than months. The connection work, testing and compliance mapping have already been done inside the platform.

Does a single point of integration help with DORA and Consumer Duty?

It cannot guarantee compliance. What it can do is simplify ICT third-party risk mapping, centralise incident reporting and produce the consistent data trails regulators expect when assessing fair customer outcomes.

Can smart routing realistically lift approval rates?

Yes. Implementations across Europe have shown that smart routing can noticeably improve authorisation rates by directing each transaction to the processor most likely to approve it. Results vary by vertical and traffic profile.

How does orchestration help manage rising first-party misuse and chargebacks?

It consolidates transaction data, risk scores and authentication logs in one place, which makes it faster to spot patterns, build evidence and adjust routing before ratios approach Visa or Mastercard monitoring thresholds.

Is network tokenisation necessary in 2026?

It is not mandated everywhere, but it has been shown to reduce fraud and improve authorisation rates. Orchestrators with provider-agnostic vaults let merchants keep control of tokens while routing freely.

Will this approach support real-time payments and future agentic commerce?

Yes. The single integration layer can ingest SEPA Instant flows and emerging machine-to-machine protocols without forcing merchants to rebuild backend connections.

Conclusion

Finera provides exactly this: one secure API, intelligent routing across a global acquirer network, built-in fraud protection and real-time analytics, so European merchants and operators can put engineering effort into growth rather than integration.

If you are reviewing your payment stack for 2026 and beyond, the useful next step is to test how a unified orchestration layer performs against your current multi-connection reality.

DISCLAIMER

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

.avif)

Frequently Asked Questions

A gateway typically connects to one or a small set of acquirers, which leaves a single point of failure. Orchestration sits above multiple gateways and acquirers, with one API for the merchant plus intelligent routing, failover and unified analytics on top.

New local APMs or acquirers are commonly onboarded in days rather than months. The connection work, testing and compliance mapping have already been done inside the platform.

It cannot guarantee compliance. What it can do is simplify ICT third-party risk mapping, centralise incident reporting and produce the consistent data trails regulators expect when assessing fair customer outcomes.

Yes. Implementations across Europe have shown that smart routing can noticeably improve authorisation rates by directing each transaction to the processor most likely to approve it. Results vary by vertical and traffic profile.

It consolidates transaction data, risk scores and authentication logs in one place, which makes it faster to spot patterns, build evidence and adjust routing before ratios approach Visa or Mastercard monitoring thresholds.

It is not mandated everywhere, but it has been shown to reduce fraud and improve authorisation rates. Orchestrators with provider-agnostic vaults let merchants keep control of tokens while routing freely.

Yes. The single integration layer can ingest SEPA Instant flows and emerging machine-to-machine protocols without forcing merchants to rebuild backend connections.

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!