Checkout Optimisation Powered by Payment Infrastructure

Checkout optimisation starts below the interface. Here is what payment infrastructure actually does.

Checkout abandonment is estimated to cost online businesses billions in lost revenue each year.The instinctive response is to redesign the form, shorten the journey, or add a progress bar. These changes matter, but they address the surface. The more consequential driver of checkout performance sits underneath the interface entirely.

Payment infrastructure determines whether a transaction succeeds or fails, how long it takes to authorise, which payment methods a customer can use, and how seamlessly security checks are handled. Get those elements wrong, and UX refinement alone may not be sufficient to recover the conversion rate.

Understanding this distinction changes where businesses focus their optimisation efforts. The interface is visible. The infrastructure is not. But the infrastructure often plays a significant role in whether conversion succeeds or fails.

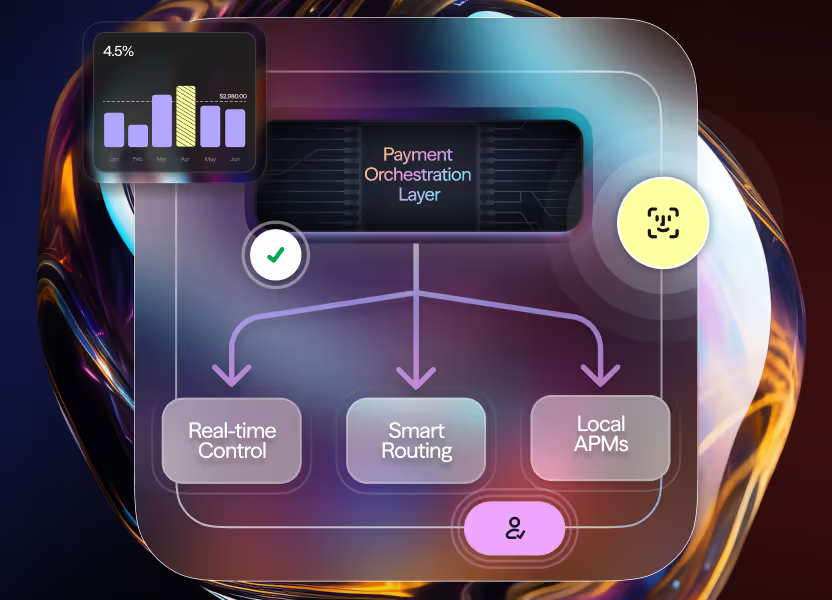

The hidden role of payment infrastructure

When a customer completes a checkout and clicks pay, several processes happen in rapid succession. The transaction is routed to an acquirer, assessed for fraud risk, submitted for authorisation, and returned with a success or failure message. The entire sequence should take seconds.

The problem is that this chain involves multiple parties, each with their own performance characteristics, regional capabilities, and failure rates. A single-provider setup means a merchant has no fallback when that provider underperforms. A poorly configured fraud filter means legitimate transactions get blocked. A routing layer that does not account for geography or card type means avoidable declines.

None of these failures are visible in the checkout interface. They show up in the conversion data.

How routing logic impacts conversion

Smart routing is one of the more impactful tools a merchant can use to influence approval rates. Rather than sending every transaction to a single acquirer by default, routing logic evaluates each transaction in real time, using factors like card type, issuing bank, geography, transaction value, and live acquirer performance.

The result is that transactions take the path most likely to result in approval. If one acquirer is underperforming or unavailable, the transaction is automatically redirected before the customer sees a failure message. For high-volume merchants, the cumulative impact of even marginal improvements to approval rates can be significant.

Routing also affects cost. Processing fees vary by acquirer, by card type, and by currency. A routing layer that optimises for both performance and cost simultaneously creates a compounding advantage over time.

The importance of local payment methods

Approval rates are not uniform across markets. Card-based payment behaviour varies significantly by country, shaped by local banking infrastructure, regulatory frameworks, and consumer habits. In markets where cards are not the primary payment method, a checkout that offers only card processing is structurally disadvantaged.

Local and alternative payment methods close this gap. Blik in Poland, UPI in India, iDEAL in the Netherlands, PIX in Brazil. These are not optional extras for merchants with global ambitions. They can be a key factor in whether a checkout performs well locally or creates unnecessary friction.

The challenge is integration. Each new payment method traditionally requires a separate contract, technical integration, and ongoing maintenance. A payment orchestration layer removes this complexity by making a catalogue of local payment methods accessible through a single integration, with the same routing and analytics applied across all of them.

Reducing friction without increasing fraud

3DS authentication introduces friction. In many markets and transaction types, it is also legally required. The tension between security compliance and conversion optimisation is real, but it is manageable.

3DS2 improves on its predecessor by enabling data sharing between merchants and card networks, which supports stronger risk assessment without necessarily triggering a challenge step for every transaction. For low-risk transactions, this means frictionless authentication. For higher-risk transactions, the challenge step provides the appropriate level of verification.

Getting this balance right requires configuration and ongoing monitoring. Challenge rates that are too high indicate overly conservative fraud settings. Excessive declines from fraud filters may mean the rules are not calibrated to the merchant's actual traffic profile. Real-time analytics allow merchants to identify these patterns and adjust accordingly.

Real-time visibility and performance tracking

Checkout optimisation is not a project with a finish line. It is a continuous process, and it requires data to be effective.

Real-time payment analytics give merchants visibility into where transactions are succeeding, where they are failing, and why. Which acquirers are performing below expectations. Which payment methods are seeing higher abandonment at checkout. Which geographies are generating unusual decline patterns.

This visibility makes optimisation deliberate rather than reactive. Instead of waiting for conversion reports to flag a problem, merchants can identify issues as they emerge and address them before they compound.

A payment infrastructure layer that consolidates data across all providers and payment methods, rather than fragmenting it across separate dashboards, makes this level of oversight practical at scale.

Infrastructure that scales globally

A checkout experience that works well in one market may perform poorly in another. Processing in new currencies, complying with local regulations, offering regionally preferred payment methods, and maintaining consistent authorisation rates across different acquiring environments all require infrastructure designed for geographic flexibility.

Merchants expanding into new markets often underestimate the payment complexity involved. A single integration that provides access to a multi-acquirer network, a broad local payment method catalogue, and real-time routing logic allows merchants to enter new geographies without rebuilding their payment stack each time.

With the right orchestration layer, the underlying integration remains consistent while the configuration adapts. That distinction is what makes global checkout performance achievable without a proportional increase in engineering overhead.

Checkout performance starts with infrastructure

Improving checkout conversion is a legitimate business priority. But solving it at the interface layer alone leaves most of the opportunity untouched.

Smart routing, multi-acquirer flexibility, local payment method coverage, calibrated fraud controls, and real-time analytics are the infrastructure conditions that determine whether a checkout succeeds. When that infrastructure is well designed, it can help improve conversion across the markets a merchant operates in.

At finera., we help merchants simplify payment complexity through orchestration, smart routing, local payment method coverage, and multi-provider infrastructure built for global scale.

If you are looking to improve payment performance, reduce checkout abandonment, or strengthen approval rates, talk to our team.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

- No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

.avif)

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!