5 Trends for a Future-Ready Payment Stack

Explore five essential capabilities every future-ready payment stack needs.

Payments are evolving rapidly, with significant changes observed in recent years. Consumer expectations are changing and new payment technologies are becoming mainstream across markets. For businesses operating online, the question is no longer whether payments infrastructure needs to evolve, but how quickly it can adapt.

An optimised payment stack for the future is not defined by a single technology or payment method. Instead, it is built on a set of core capabilities that allow businesses to scale, localise, and manage risk effectively as markets, regulations and customer behaviour change.

Five current payment trends define a future-ready payment stack.

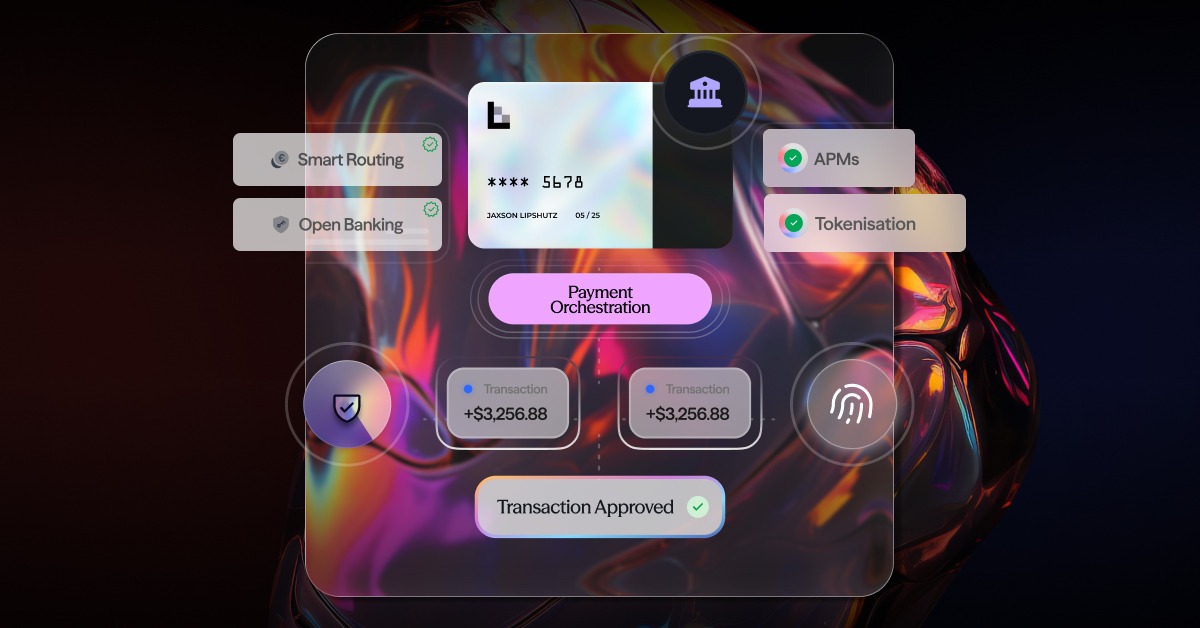

1. Strong Coverage of Alternative Payment Methods (APMs)

Cards remain important, but they are no longer sufficient on their own. Across many regions, consumers increasingly prefer alternative payment methods that align with local habits, banking infrastructure, and mobile usage.

Industry research indicates that alternative payment methods represent a growing share of global e-commerce transactions, with adoption observed across Europe, Asia and high-growth markets.

APMs such as local bank transfers, real-time payments, wallets and QR-based methods reduce friction by offering familiarity and trust. When customers see a payment method they already use in daily life, the checkout experience may feel more familiar and intuitive.

A future-ready payment stack should support a broad and evolving APM portfolio, allowing businesses to adapt as local preferences change rather than relying on a fixed set of payment options.

2. Open Banking and Bank-Based Payment Connectivity

Open banking is becoming a foundational layer in modern payments. It enables direct, account-to-account payments authorised through a user’s bank, often with strong authentication and real-time confirmation.

In Europe, open banking adoption continues to expand under PSD2, while similar frameworks are emerging in markets such as the UK, Australia and parts of Asia. According to McKinsey research, account-to-account payments are expected to experience growth as some consumers seek alternatives to cards.

For businesses, open banking can support payments and may reduce reliance on card networks. Importantly, open banking does not replace other payment methods; it complements them.

A future-ready payment stack is one that seamlessly blends bank-based payments with cards, wallets, and other Alternative Payment Methods (APMs).

3. Payment Orchestration for Scale and Flexibility

As payment stacks grow more complex, orchestration may become increasingly important. Without it, businesses face fragmented integrations, inconsistent reporting, and operational overhead as they expand into new regions or add new methods.

Payment orchestration provides a layer that connects multiple payment providers, acquirers and methods through a single integration.

From a future-readiness perspective, orchestration may support:

- Faster expansion into new markets without rebuilding payment flows.

- Smarter routing across providers based on geography or method.

- Reduced dependency on a single provider.

- Centralised visibility across transactions and performance.

For many businesses, orchestration is becoming an important component of scalable payment infrastructure.

4. Faster and More Flexible Payout Capabilities

Payout speed can be an important consideration alongside payout reliability. Faster access to funds is increasingly expected in sectors such as ecommerce, marketplaces, digital services and iGaming.

Research from Deloitte suggests that faster payouts may influence user satisfaction and platform trust in certain contexts, particularly where users depend on timely access to funds.

A future-ready payment stack supports multiple payout methods and allows businesses to decide when faster payouts are appropriate, rather than applying a single approach to all users or regions.

5. Built-In Security and Fraud Detection

As payments become more diverse, security and compliance must scale alongside them. Fraud risks vary by market, method and transaction type, making one-size-fits-all controls ineffective.

According to the European Central Bank, strong customer authentication and transaction monitoring are important considerations as digital payment volumes increase.

A future-ready payment stack may include support for strong authentication standards, tokenisation and secure data handling, fraud detection and monitoring across providers.

Security should be embedded into the payment infrastructure rather than added as an afterthought.

Optimise Your Payment Stack with finera.

Optimised payments are not about predicting a single winning method or technology. They are about building infrastructure that can adapt as consumer behaviour, regulation and payment innovation evolve.

Payment infrastructure that combines APM diversity, open banking connectivity, orchestration, flexible payouts and embedded security may be better positioned to support long-term growth and reduce the need for repeated re-engineering.

Whether you are expanding into new regions, optimising payout flows, or strengthening your overall payment strategy, the right foundation is an important consideration.

Considering building a future-ready payment stack? Contact our team to explore how finera’s payment orchestration services may support your business needs.

This article on payment methods is for informational and educational purposes only.

- Not Professional Advice: The content provided does not constitute financial, legal, tax, or professional advice. Always consult with a qualified professional before making financial decisions.

- No Liability: The authors, contributors, and the publisher assume no liability for any loss, damage, or consequence whatsoever, whether direct or indirect, resulting from your reliance on or use of the information contained herein.

- Third-Party Risk: The discussion of specific payment services, platforms, or institutions is for illustration only. We do not endorse or guarantee the performance, security, or policies of any third-party service mentioned. Use all third-party services at your own risk.

No Warranty: We make no warranty regarding the accuracy, completeness, or suitability of the information, which may become outdated over time.

.avif)

Frequently Asked Questions

Still Have Questions?

Let’s Find the Right Solution for You

Stay Connected with Us!

Follow us on social media to stay up to date with the latest news, updates, and exclusive insights!

-thumbnail.avif)

.avif)